Introduction

在线阅读地址:https://caterpillarstudygroup.github.io/LiuYuBo_ML_pages/

《python3入门机器学习 经典算法与应用》学习笔记

视频资源链接:https://coding.imooc.com/class/169.html

这套视频课系列原作者刘宇波。课程发布于慕课网。

课程对常见机器学习算法做了基础的介绍。既有原理也有编程实践。还有一些对算法的思考。

在讲原理有少量的数学推导,数学基础不好也能看懂。

简单的算法配有python3实现,复杂算法使用slearn观察算法效果,对算法有直观印象。

适用于机器学习入门,也可用于熟悉python、numpy和sklearn。

这个系列课程不错,墙裂推荐

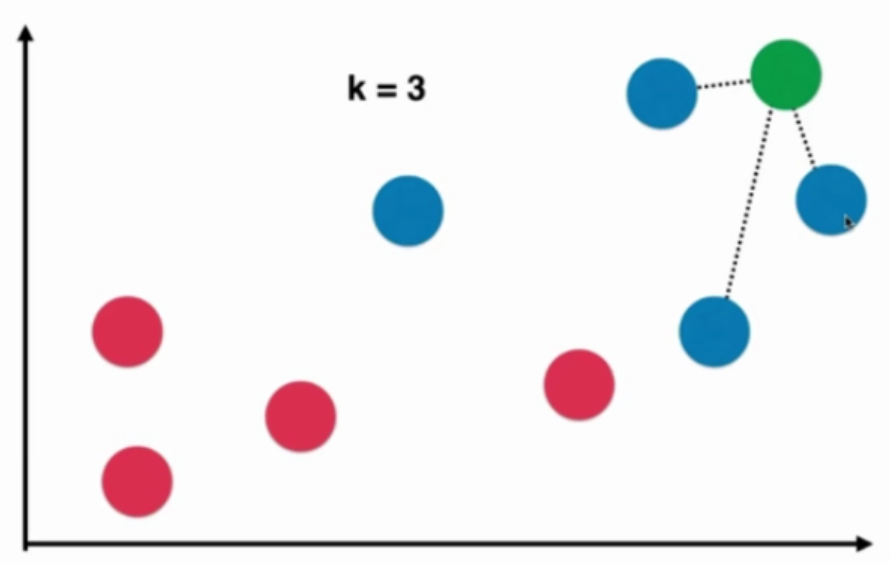

KNN - K近邻算法 - K-Nearest Neighbors

KNN算法是非常适合入门机器学习的算法,因为

- 思想极度简单

- 应用数学知识少

- 效果好

- 可以解释机器学习算法使用过程中的很多细节问题

- 更完整地刻画机器学习应用的流程

2019-10-19

KNN - K近邻算法 - K-Nearest Neighbors

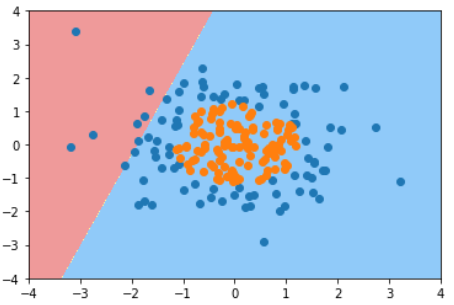

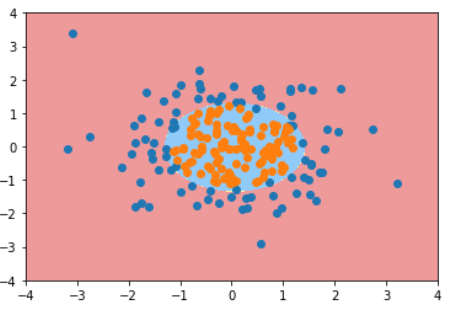

本质:如果两个样本足够相似,它们有更高的概率属于同一个类别

代码实现KNN算法

假设原始训练数据如下:

raw_data_X = [[3.39, 2.33],

[3.11, 1.78],

[1.34, 3.36],

[3.58, 4.67],

[2.28, 2.86],

[7.42, 4.69],

[5.74, 3.53],

[9.17, 2.51],

[7.79, 3.42],

[7.93, 0.79]

]

raw_data_y = [0, 0, 0, 0, 0, 1, 1, 1, 1, 1]

待求数据如下:

x = np.array([8.09, 3.36])

数据准备

import numpy as np

import matplotlib.pyplot as plt

X_train = np.array(raw_data_X)

y_train = np.array(raw_data_y)

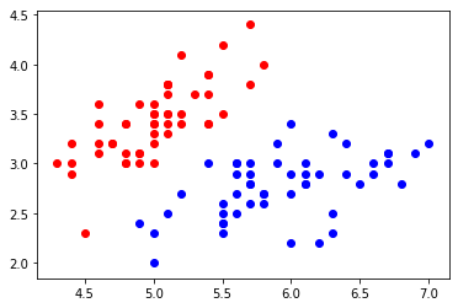

plt.scatter(X_train[y_train==0, 0], X_train[y_train==0, 1], color = 'g')

plt.scatter(X_train[y_train==1, 0], X_train[y_train==1, 1], color = 'r')

plt.scatter(x[0], x[1], color = 'b')

plt.show()

效果:

KNN过程

欧拉距离

假设有a, b两个点,平面中两个点之间的欧拉距离为:

$$ \sqrt {(x^{(a)}-x^{(b)})^2+(y^{(a)}-y^{(b)})^2} $$

立体中两个点的欧拉距离为:

$$ \sqrt {(x^{(a)}-x^{(b)})^2+(y^{(a)}-y^{(b)})^2+(z^{(a)}-z^{(b)})^2} $$

任意维度中两个点的欧拉距离为:

$$ \sqrt {(X^{(a)}_1-X^{(b)}_1)^2+ (X^{(a)}_2-X^{(b)}_2)^2+...+(X^{(a)}_n-X^{(b)}_n)^2} $$

或

$$ \sqrt {\sum^n_{i=1} (X^{(a)}_i-X^{(b)}_i)^2} $$

其中上标a, b代码第a, b个数据。下标1, 2代码数据的第1, 2个特征

代码如下:

distances = [np.sum((x_train - x) ** 2) for x_train in X_train]

nearest = np.argsort(distances)

topK_y = [y_train[i] for i in nearest[:k]]

from collections import Counter

votes = Counter(topK_y)

predict_y = votes.most_common(1)[0][0]

运行结果:predict_y = 1

代码实现KNN算法

import numpy as np

from math import sqrt

from collections import Counter

def kNN_classify(k, X_train, y_train, x):

assert 1 <= k <= X_train.shape[0], "k must be valid"

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must equal to the size of y_train"

assert X_train.shape[1] == x.shape[0], "the feature number of x must be equal to X_train"

distances = [sqrt(np.sum((x_train-x)**2)) for x_train in X_train]

nearst = np.argsort(distances)

topK_y = [y_train[i] for i in nearst[:k]]

votes = Counter(topK_y)

return votes.most_common(1)[0][0]

准备数据

import numpy as np

raw_data_X = [[3.39, 2.33],

[3.11, 1.78],

[1.34, 3.36],

[3.58, 4.67],

[2.28, 2.86],

[7.42, 4.69],

[5.74, 3.53],

[9.17, 2.51],

[7.79, 3.42],

[7.93, 0.79]

]

raw_data_y = [0, 0, 0, 0, 0, 1, 1, 1, 1, 1]

X_train = raw_data_X

y_train = raw_data_y

x = np.array([8.09, 3.36])

调用算法

predict_y = kNN_classify(6, X_train, y_train, x)

运行结果:predict_y = 1

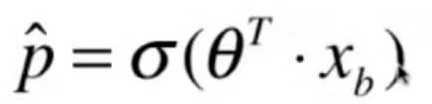

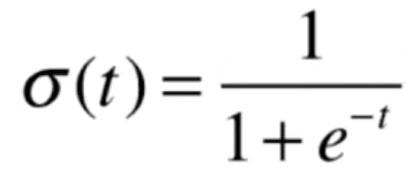

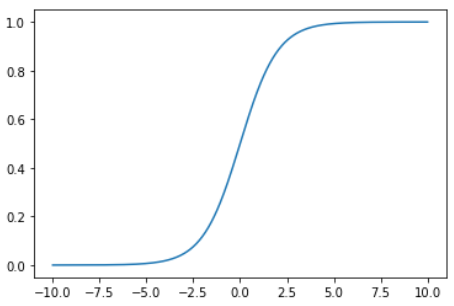

什么是机器学习

KNN是一个不需要训练的算法

KNN没有模型,或者说训练数据就是它的模型

使用scikit-learn中的kNN

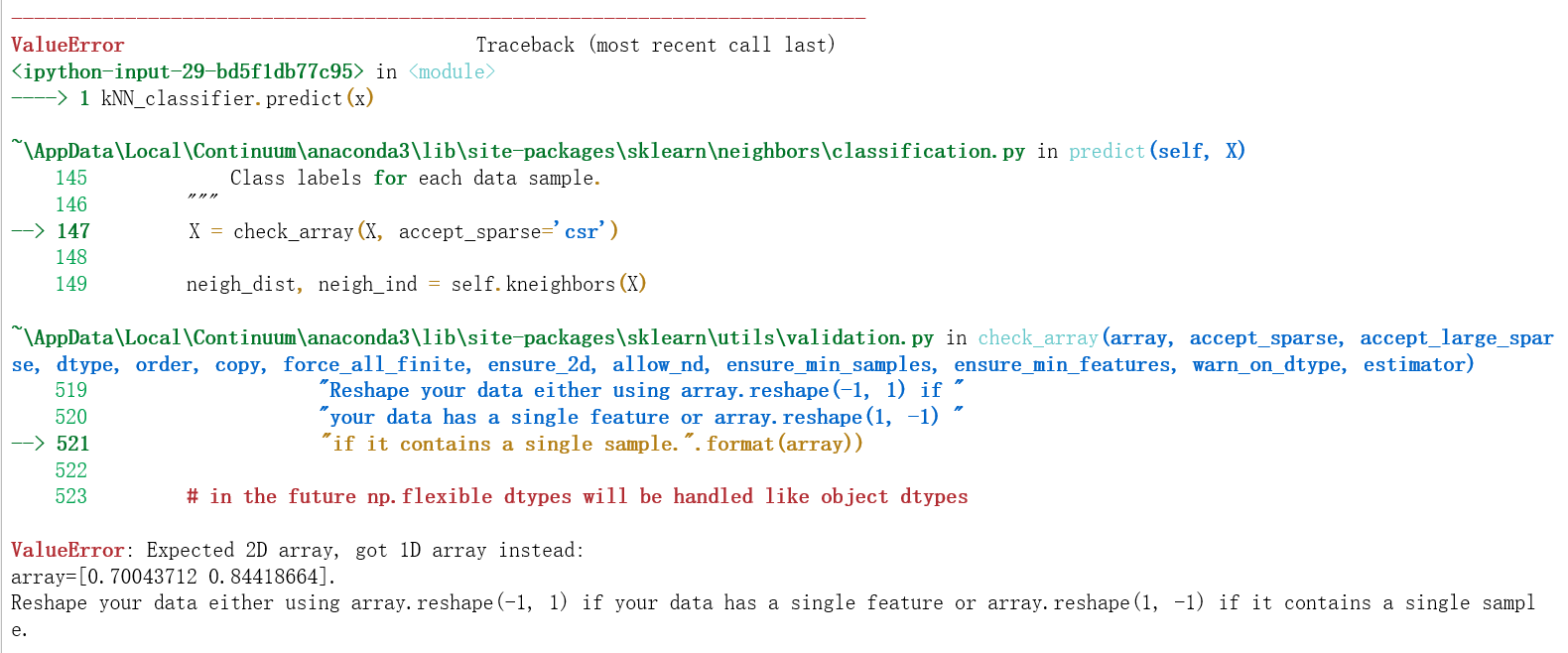

错误写法

from sklearn.neighbors import KNeighborsClassifier

kNN_classifier.fit(X_train, y_train)

kNN_classifier.predict(x)

这样写会报错:

原因是,predict为了兼容多组测试数据的场景,要求参数是个矩阵

正确写法

from sklearn.neighbors import KNeighborsClassifier

kNN_classifier.fit(X_train, y_train)

X_predict = x.reshape(1, -1)

y_predict = kNN_classifier.predict(X_predict)

运行结果:predict_y[0] = 1

重新整理我们的kNN的代码

封装成sklearn风格的类

import numpy as np

from math import sqrt

from collections import Counter

class kNNClassifier:

def __init__(self, k):

"""初始化kNN分类器"""

assert k >= 1, "K must be valid!"

self.k = k

self._X_train = None

self._y_train = None

def fit(self, X_train, y_train):

"""根据训练数据集X_train和y_train训练kNN分类器"""

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must equal to the size of y_train"

assert self.k <= X_train.shape[0], "the size of X_train must be at least k"

self._X_train = X_train

self._y_train = y_train

return self

def predict(self, X_predict):

"""给定待预测数据集X_predict, 返回表示X_predict的结果向量"""

assert self._X_train is not None and self._X_train is not None, "must fit before predict"

assert self._X_train.shape[1] == X_predict.shape[1], "the feature number of X_predict must be equal to X_train"

y_predict = [self._predict(x) for x in X_predict]

return np.array(y_predict)

def _predict(self, x):

"""给定单个待测数据x,返回x的预测结果"""

assert self._X_train.shape[1] == x.shape[0], "the feature number of x must be equal to X_train"

distances = [sqrt(np.sum((x_train-x)**2)) for x_train in self._X_train]

nearst = np.argsort(distances)

topK_y = [self._y_train[i] for i in nearst[:self.k]]

votes = Counter(topK_y)

return votes.most_common(1)[0][0]

def __repr__(self):

return "KNN(k=%d)" % self.k

使用kNNClassifier

knn_clf = kNNClassifier(k=6)

knn_clf.fit(X_train, y_train)

y_predict = knn_clf.predict(X_predict)

运行结果:predict_y[0] = 1

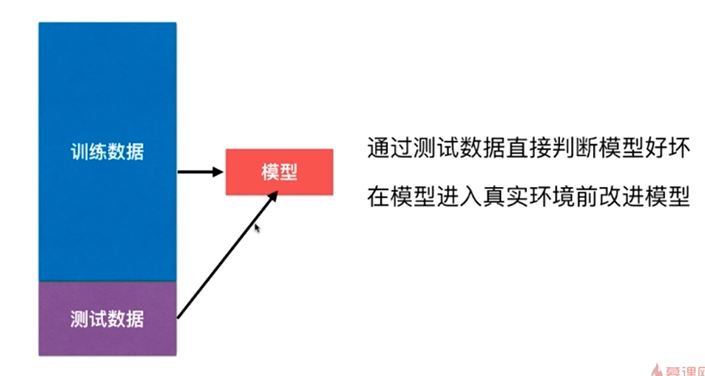

判断机器学习算法的性能

改进:训练和测试数据集的分离,train test split

但这种方式也有它的问题,后面其它小节会讲到

准备iris数据

import numpy as np

import matplotlib.pyplot as plt

from sklearn import datasets

iris = datasets.load_iris()

X = iris.data

y = iris.target

X.shape为(150, 4),y.shape为(150,)

train_test_split

注意1:本例中训练数据集的为如下:

因此按顺序取前多少个样本不会有很好的效果,要先对数据乱序化

注意2:本例中X和y是分离的,但它们不能分别乱序化。乱序化的同时要保证样本和标签是对应的。

在Notebook实现

shuffle_indexes = np.random.permutation(len(X))

test_ratio = 0.2

test_size = int(len(x) * test_ratio)

test_indexes = shuffle_indexes[:test_size]

train_indexes = shuffle_indexes[test_size:]

X_train = X[train_indexes]

y_train = y[train_indexes]

X_test = X[test_indexes]

y_test = y[test_indexes]

将train_test_split封装成函数

import numpy as np

def train_test_split(X, y, test_ratio=0.2, seed=None):

"""将X和y按照test_ratio分割成X_train,X_test,y_train,y_test"""

assert X.shape[0] == y.shape[0], "the size of X must be equal to the size of y"

assert 0.0 <= test_ratio <= 1.0, "test_ration must be valid"

if seed:

np.random.seed(seed)

shuffle_indexes = np.random.permutation(len(X))

test_size = int(len(x) * test_ratio)

test_indexes = shuffle_indexes[:test_size]

train_indexes = shuffle_indexes[test_size:]

X_train = X[train_indexes]

y_train = y[train_indexes]

X_test = X[test_indexes]

y_test = y[test_indexes]

return X_train, X_test, y_train, y_test

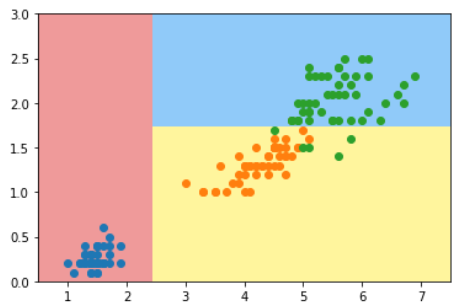

KNN结合train_test_split计算分类准确度

X_train, X_test, y_train, y_test = train_test_split(X, y)

my_Knn_clf = kNNClassifier(k = 3) # kNNClassifier在上一节实现

my_Knn_clf.fit(X_train, y_train)

y_predict = my_Knn_clf.predict(X_test)

accuracy = sum(y_predict == y_test) / len(y_test)

sklearn中的train_test_split

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=666)

在4-3中使用了分类准确度accuracy来评判KNN算法的性能。

使用accuracy来评价KNN算法对手写数据集的分类效果

加载手写数据集

from sklearn import datasets

digits = datasets.load_digits()

digits的内容如下:

输入:digits.keys()

输出:dict_keys(['data', 'target', 'target_names', 'images', 'DESCR'])

输入:print(digits.DESCR)

输出:digits的官方说明

输入:digits.data.shape()

输出:(1797, 64)

输入:digits.target.shape()

输出:(1797,)

输入:digits.target_names

输出:array([0, 1, 2, 3, 4, 5, 6, 7, 8, 9])

输入:

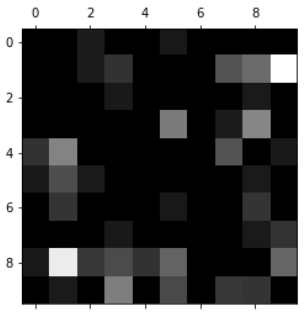

some_digit = X[666]

some_digit_image = some_digit.reshape(8, 8)

plt.imshow(some_digit_image, cmap = matplotlib.cm.binary)

plt.show()

输出:第666个样本的图像

train_test_split + KNN + accuracy

import numpy as np

import matplotlib

import matplotlib.pyplot as plt

from sklearn import datasets

digits = datasets.load_digits()

X = digits.data

y = digits.target

X_train, X_test, y_train, y_test = train_test_split(X, y, test_ratio=0.2)

my_knn_clf = KNNClassifier(k=3)

my_knn_clf.fit(X_train, y_train)

y_predict = my_knn_clf.predict(X_test)

accuracy = sum(y_predict == y_test) / len(y_test)

scikit-learn中的accuracy_score

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=666)

from sklearn.neighbors import KNeighborsClassifier

knn_clf = KNeighborsClassifier(n_neighbors=3)

knn_clf.fit(X_train, y_train)

y_predict = knn_clf.predict(X_test)

from sklearn.metrics import accuracy_score

accuracy = accuracy_score(y_test, y_predict)

超参数和模型参数

超参数是指运行机器学习算法之前要指定的参数

KNN算法中的K就是一个超参数

模型参数:算法过程中学习的参数

KNN算法没有模型参数

调参是指调超参数

如何寻找好的超参数

- 领域知识

- 经验数值

- 实验搜索

寻找最好的K

best_score = 0.0

best_k = -1

for k in range(1, 11):

knn_clf = KNeighborsClassifier(n_neighbors=k)

knn_clf.fit(X_train, y_train)

score = knn_clf.score(X_test, y_test)

if score > best_score:

best_k = k

best_score = score

print("best_k = ", best_k)

print("best_score = ", best_score)

输出:

best_k = 4

best_score = 0.9916666666666667

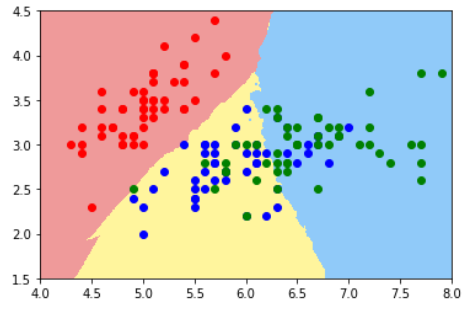

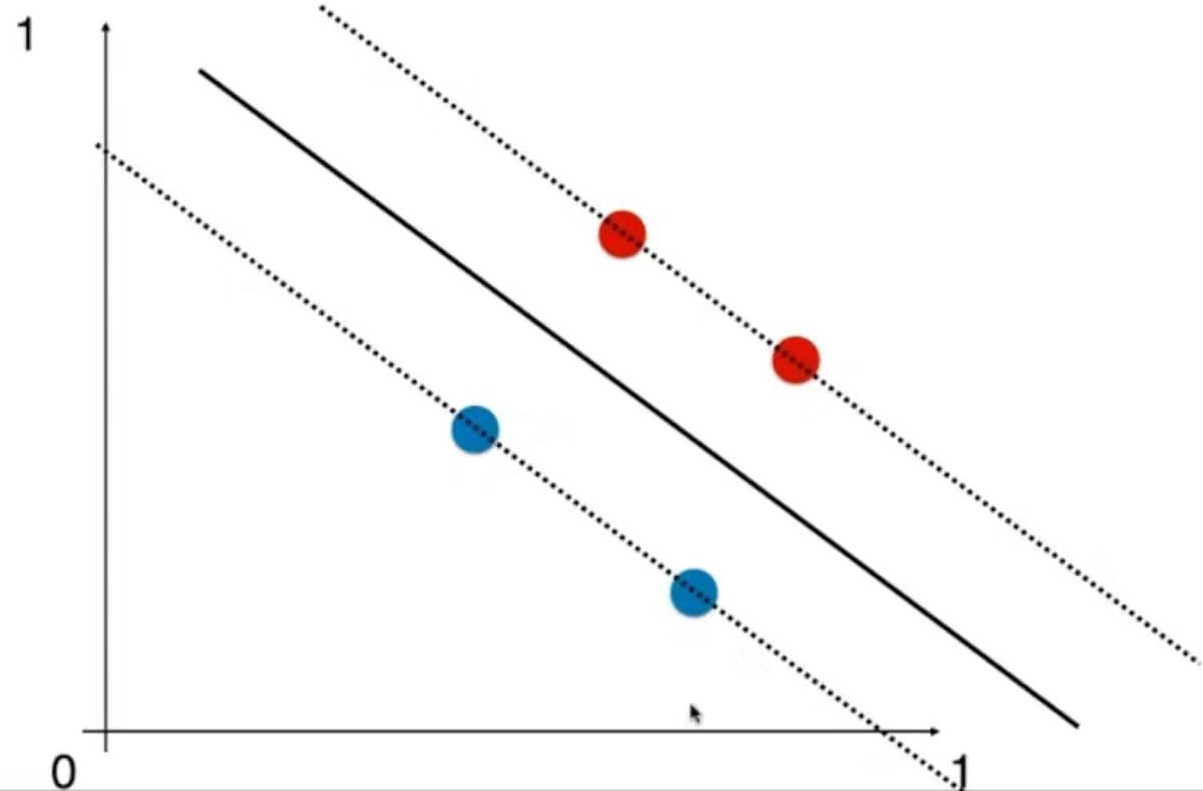

KNN的超参数weights

-

普通的KNN算法:蓝色获胜

-

考虑距离的KNN算法:红色:1, 蓝色:1/3 + 1/4 = 7/12,蓝色获胜

考虑距离的另一个优点:解决平票的情况

best_method = ""

best_score = 0.0

best_k = -1

for method in ["uniform", "distance"]:

for k in range(1, 11):

knn_clf = KNeighborsClassifier(n_neighbors=k, weights=method)

knn_clf.fit(X_train, y_train)

score = knn_clf.score(X_test, y_test)

if score > best_score:

best_k = k

best_score = score

best_method = method

print("best_k = ", best_k)

print("best_score = ", best_score)

print("best_method = ", best_method)

输出结果:

best_k = 4

best_score = 0.9916666666666667

best_method = uniform

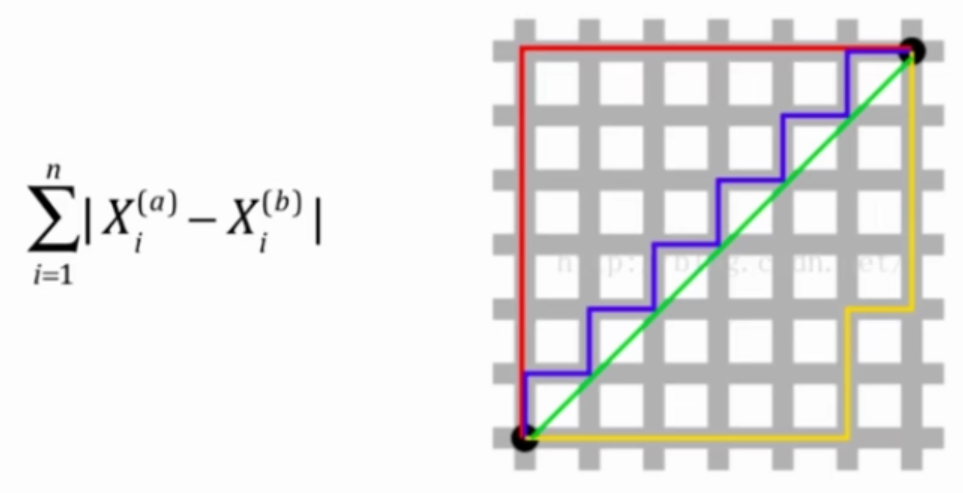

KNN的超参数p

关于距离的更多定义

- 欧拉距离

$$ \sqrt {\sum^n_{i=1} (X^{(a)}_i-X^{(b)}_i)^2} $$

- 曼哈顿距离

- 欧拉距离与曼哈顿距离的数学形式一致性

$$ (\sum^n_{i=1} |X^{(a)}_i-X^{(b)}_i|^2)^\frac{1}{2} $$

$$ (\sum^n_{i=1} |X^{(a)}_i-X^{(b)}_i|)^\frac{1}{1} $$

- 明可夫斯基距离 Minkowski distance

$$ (\sum^n_{i=1} |X^{(a)}_i-X^{(b)}_i|^p)^\frac{1}{p} $$

把欧拉距离和曼哈顿距离进一步抽象,得到以下公式

p = 1: 曼哈顿距离

p = 2: 欧拉距离

p > 2: 其他数学意义

%%time

best_p = -1

best_score = 0.0

best_k = -1

for k in range(1, 11):

for p in range(1, 6):

knn_clf = KNeighborsClassifier(n_neighbors=k, weights="distance", p = p)

knn_clf.fit(X_train, y_train)

score = knn_clf.score(X_test, y_test)

if score > best_score:

best_k = k

best_score = score

best_p = p

print("best_k = ", best_k)

print("best_score = ", best_score)

print("best_p = ", best_p)

输出结果:

best_k = 3

best_score = 0.9888888888888889

best_p = 2

Wall time: 37 s

Grid Search

准备数据

from sklearn import datasets

digits = datasets.load_digits()

X = digits.data

y = digits.target

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=666)

使用网格搜索

from sklearn.neighbors import KNeighborsClassifier

from sklearn.model_selection import GridSearchCV

param_grid = [

{

'weights':['uniform'],

'n_neighbors': [i for i in range(1, 11)]

},

{

'weights':['distance'],

'n_neighbors': [i for i in range(1, 11)],

'p': [i for i in range(1, 6)]

}

]

knn_clf = KNeighborsClassifier()

grid_search = GridSearchCV(knn_clf, param_grid)

%%time

grid_search.fit(X_train, y_train)

输出结果:

察看运行结果

输入:grid_search.best_score_

输出:0.9853862212943633

输入:grid_search.best_params_

输出:{'n_neighbors': 3, 'p': 3, 'weights': 'distance'}

注意1:这里的搜索结果与4-5中自己编写的网格搜索得到的结果不同,是因为评价方法不同,不用care

注意2:以_结尾的参考表示为计算得到的参数,而不是用户输入的参数

使用运行结果建立新的模型

knn_clf = grid_search.best_estimator_

knn_clf.score(X_test, y_test)

输出结果: 0.9833333333333333

其它GridSearchCV参数

- njobs:使用多核计算

- verbose:中间过程的打印级别

更多的距离定义

样本间的距离被发现时间所主导

如果把发现时间改成以年为单位,样本间的距离又会被肿瘤大小所主导

如果不对样本进行预处理,样本间的距离可能会被部分特征主导

解决方案:将所有的数据映射到同一个尺度,即归一化

数据归一化 (feature scaling)

最值归一化 normalization

把所有数据映射到0-1之间

$$ x_{scale} = \frac {x - x_{min}}{x_{max} - x_{min}} $$

适用于分布有明显边界的情况,但是受outlier也就是极值(极端数据)影响较大会不准确

均值方差归一化 standardization

把所有数据归一到均值为0方差为1的分布中

$$ x_{scale} = \frac {x-x_{mean}}{S} $$

适用于数据分布没有明显的边界,有可能存在极端的数据值,其中S是标准差。由于均值方差归一化对于符合最值归一化的数据集有着同样好的归一化处理结果,所以一般推荐使用均值方差归一化方法。

代码实现归一化

最值归一化

对向量所有元素归一化

生成随机数据

x = np.random.randint(0, 100, size = 100)

归一化后

(x - np.min(x)) / (np.max(x) - np.min(x))

对矩阵元素归一化

X = np.random.randint(0, 100, (50, 2))

X = np.array(X, dtype = float)

X[:, 0] = (X[:,0] - np.min(X[:,0])) / (np.max(X[:,0])-np.min(X[:,0]))

X[:, 1] = (X[:,1] - np.min(X[:,1])) / (np.max(X[:,1])-np.min(X[:,1]))

均值方差归一化 standardization

X2 = np.random.randint(0, 100, (50, 2))

X2 = np.array(X2, dtype = float)

X2[:,0] = (X2[:,0] - np.mean(X2[:,0])) / np.std(X2[:,0])

X2[:,1] = (X2[:,1] - np.mean(X2[:,1])) / np.std(X2[:,1])

输入:np.mean(X2[:,0])

输出:7.771561172376095e-17

输入:np.std(X2[:,0])

输出:1.0

训练数据集和测试数据集不能分别归一化。

测试数据集使用与训练数据集相同的mean和std做归一化

即

(x_test - mean_train) / std_train

scikit-learn中的Scaler的使用流程

使用scikit-learn中的StandardScaler

准备数据

import numpy as np

from sklearn import datasets

iris = datasets.load_iris()

X = iris.data

y = iris.target

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(iris.data, iris.target, random_state=666)

scikit-learn中的StandardScaler

from sklearn.preprocessing import StandardScaler

standardScaler = StandardScaler()

standardScaler.fit(X_train)

X_train_standard = standardScaler.transform(X_train)

X_test_standard = standardScaler.transform(X_test)

StandardScaler + KNN + accuracy

from sklearn.neighbors import KNeighborsClassifier

knn_clf = KNeighborsClassifier(n_neighbors=3)

knn_clf.fit(X_train_standard, y_train)

knn_clf.score(X_test_standard, y_test)

自己实现StandardScaler并封装成类

import numpy as np

class StandardScaler:

def __init__(self):

self.mean_ = None

self.scale_ = None

def fit(self, X):

"""根据训练数据集X获取数据的均值和方差"""

assert X.ndim == 2, "The dimension of X must be 2"

self.mean_ = np.array([np.mean(X[:,i]) for i in range(X.shape[1])])

self.scale_ = np.array([np.std(X[:,i]) for i in range(X.shape[1])])

def transform(self, X):

"""将X根据这个StandardScaler进行均值方差归一化处理"""

assert X.ndim == 2, "The dimension of X must be 2"

assert self.mean_ is not None and self.scale_ is not None, "must fit before transform!"

retX = np.empty(shape = X.shape, type = float)

for col in range(X.shape[1]):

retX[:, col] = (X[:,col] - self.mean_[col]) / self.scale_[col]

return retX

优点:

解决分类问题,天然可以解决多分类问题

思想简单,效果强大

可以解决回归问题:KNeighborsRegressor

缺点:

效率低下,m个特征n个样本,预测一个数据的时间复杂度为O(m * n)

高度数据相关

预测结果不所有可解释性

维数灾难:随着维度的增加,看似相近的两个点距离越来越大,解决方法:降维

机器学习流程回顾

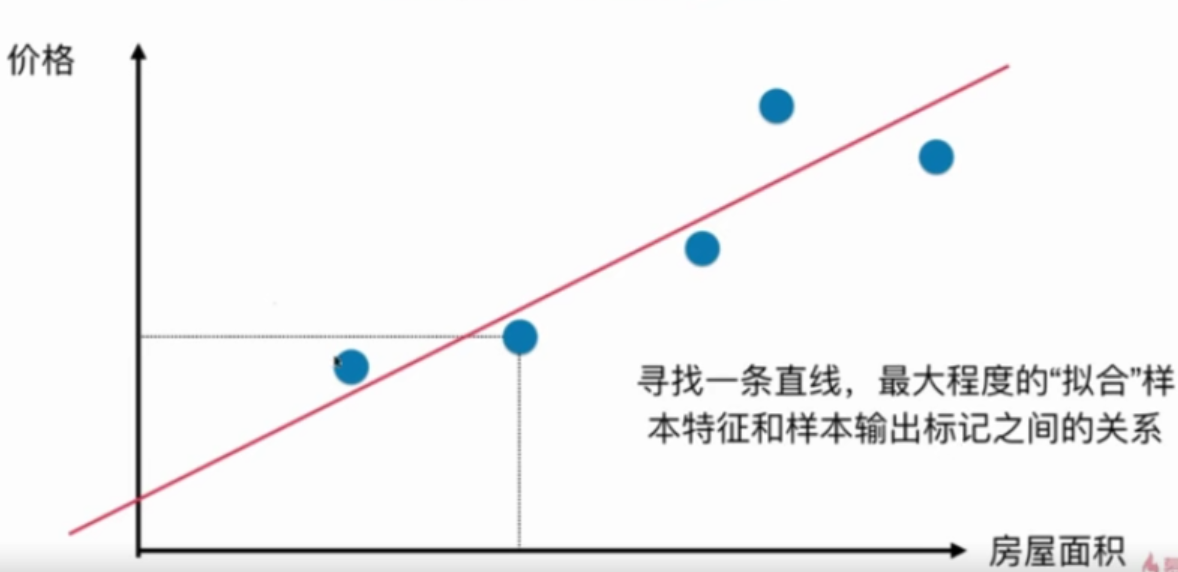

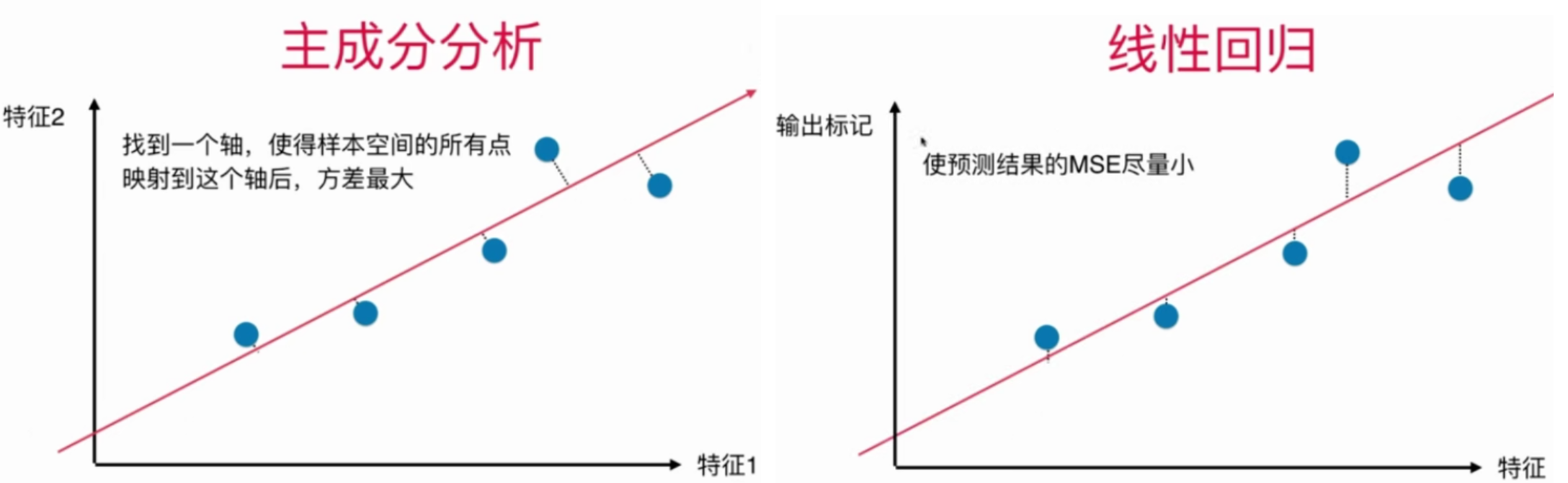

线性回归算法

解决回归问题

思想简单、实现容易

许多强大的非线性模型的基础

结果具有很好的可解释性

蕴含机器学习中的很多重要思想

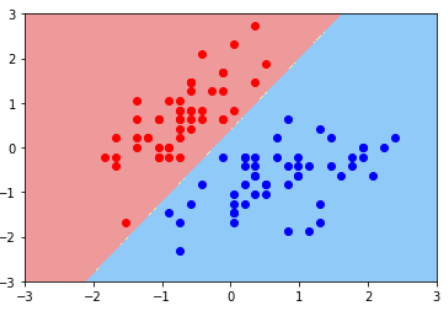

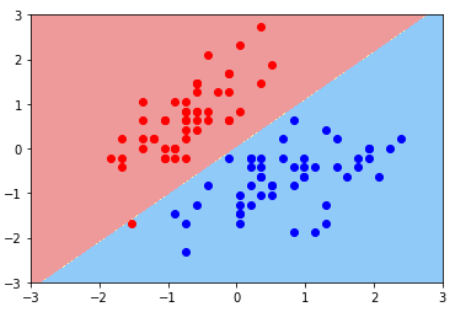

注意1:这里的二维平面图与分类问题的二维平面图不同

在分类问题中,横轴和纵轴都是样本特征,输出标记用颜色表示

在回归问题中,横轴是样本特征,纵轴是输出标记

注意2:

样本特征只有一个,称为简单线性回归

样本特征有多个,称为多元线性回归

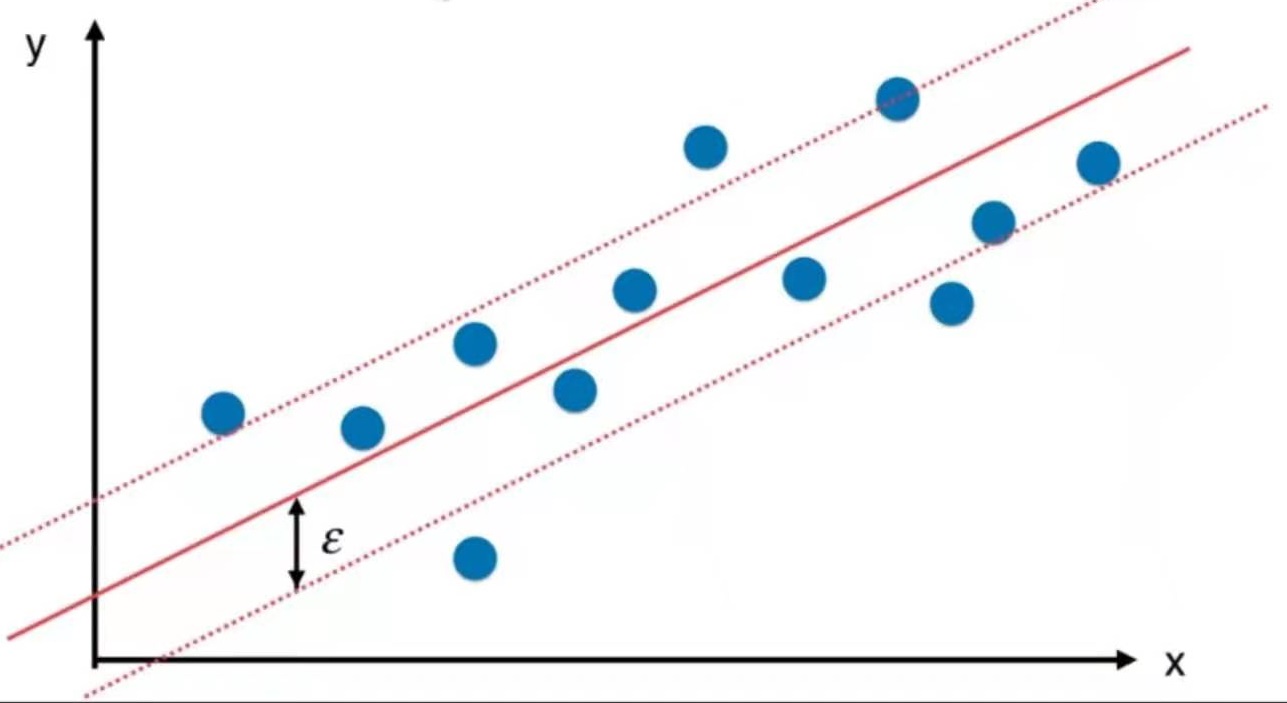

简单线性回归

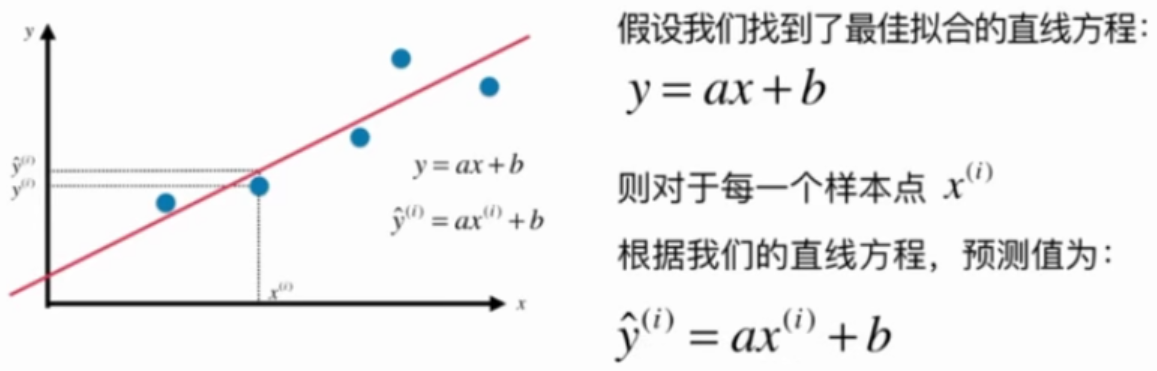

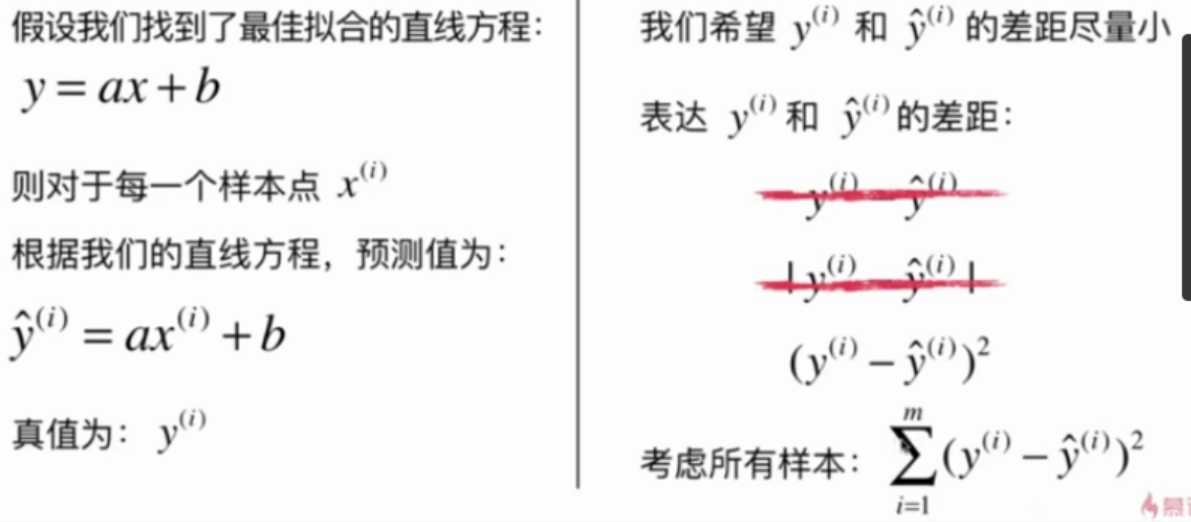

找一条直线,这条直线最大程度地拟合所有的样本特征点

一类机器学习算法的基本思路

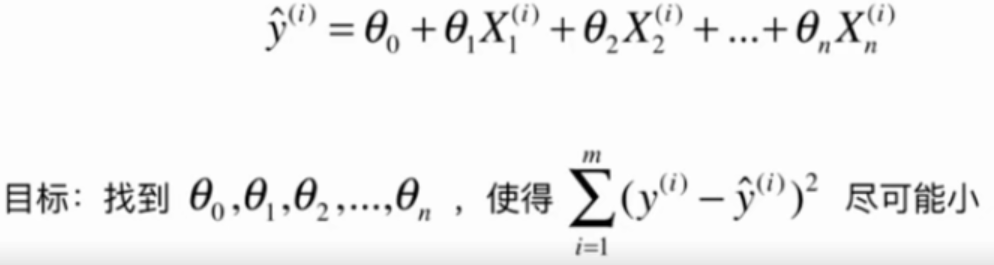

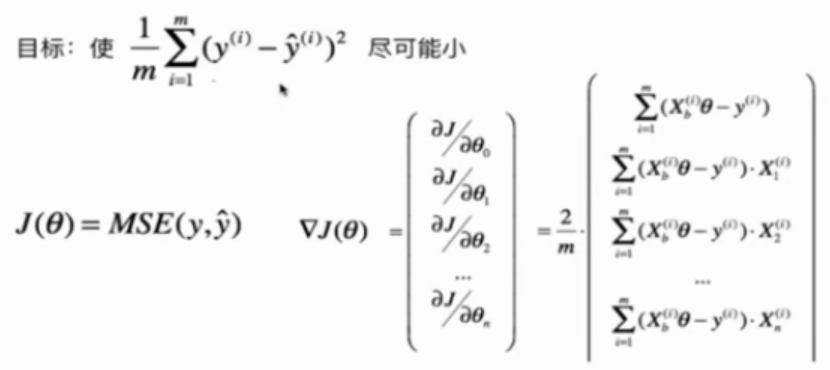

通过分析问题,确定问题的损失函数(loss function)或效用函数(utility function), 有时也称为目标函数

通过最优化损失函数或效用函数,获得机器学习的模型

近乎所有的参数学习算法都是这样的套路, e.g. 线性回归, 多项式回归, 逻辑回归, SVM, 神经网络, etc...本质都是在学习相应的参数来最优化目标函数, 区别在于模型不同从而建立的目标函数不同, 优化的方式也不尽相同.

最优化原理

凸优化

最小化本文中的损失函数

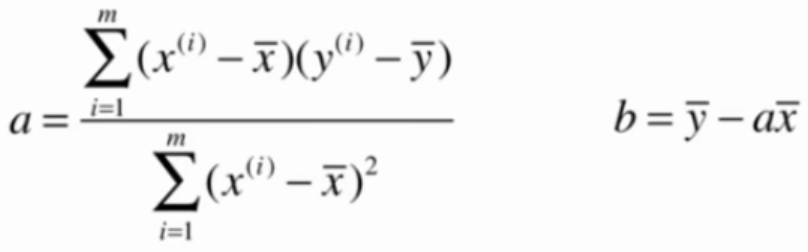

目标:找到$${a}$$和$${b}$$,使用$$\sum^m_{i=1}(y^{(i)}-ax^{(i)}-b)^2$$尽可能小。

这是典型的最小二乘法问题:最小化误差的平方

解得:

$$ a = \frac{\sum_{i=1}^m(x^{(i)}-\bar x)(y^{(i)}-\bar y)}{\sum_{i=1}^m(x^{(i)}-\bar x)^2}\quad \quad \quad \quad \quad b = \bar y - a\bar x $$

5-1中的a和b的证明过程

这一节没有做笔记

import numpy as np

import matplotlib.pyplot as plt

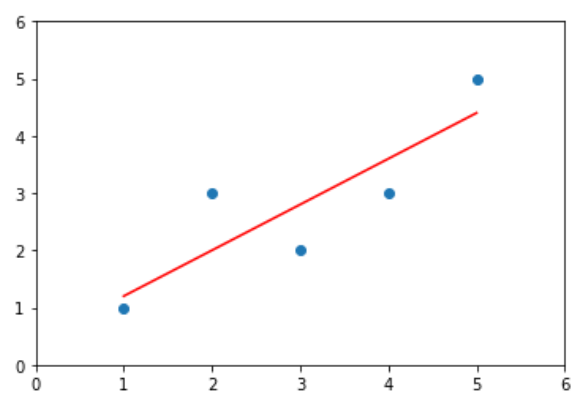

x = np.array([1., 2., 3., 4., 5.])

y = np.array([1., 3., 2.

plt.scatter(x, y)

plt.axis([0, 6, 0, 6])

plt.show()

输出结果:

在Notebook中计算a, b

计算a, b

x_mean = np.mean(x)

y_mean = np.mean(y)

num = 0.0

d = 0.0

for x_i, y_i in zip(x, y):

num += (x_i - x_mean) * (y_i - y_mean)

d += (x_i - x_mean) ** 2

a = num / d

b = y_mean - a * x_mean

绘制结果

y_hat = a * x + b

plt.scatter(x, y)

plt.plot(x, y_hat, color='r')

plt.axis([0, 6, 0, 6])

plt.show()

输出结果:

把上过程封装成类

import numpy as np

class SimpleLinearRegression1:

def __init__(self):

"""初始化Single Linear Regression模型"""

self.a_ = None

self.b_ = None

def fit(self, x_train, y_train):

"""根据训练数据集X_train, y_train训练Single Linear Regression模型"""

assert x_train.ndim == 1, "Simple Linear Regressor can only solve single feature training data"

assert len(x_train) == len(y_train), "the size of x_train must be equal to the size of y_train"

x_mean = np.mean(x_train)

y_mean = np.mean(y_train)

num = 0.0

d = 0.0

for x_i, y_i in zip(x_train, y_train):

num += (x_i - x_mean) * (y_i - y_mean)

d += (x_i - x_mean) ** 2

self.a_ = num / d

self.b_ = y_mean - self.a_ * x_mean

def predict(self, x_predict):

"""给定待测数据集X_predict,返回表示x_predict的结果向量"""

assert x_predict.ndim == 1, "Simple Linear Regressor can only solve single feature training data"

assert self.a_ is not None and self.b_ is not None, "must fit before predict"

return [self._predict(x) for x in x_predict]

def _predict(self, x_single):

"""给定单个待预测数据s_single,返回x_single的预测结果"""

return self.a_ * x_single + self.b_

def __repr__(self):

return "SimpleLinearRegression1()"

训练模型

reg1 = SimpleLinearRegression1()

reg1.fit(x, y)

绘制结果

y_hat1 = a * x + b

plt.scatter(x, y)

plt.plot(x, y_hat1, color='r')

plt.axis([0, 6, 0, 6])

plt.show()

输出结果:

5-3中计算a, b的实现方法性能较低,使用向量化运算能提高性能

即把以下公式向量化:

向量化的依据:

向量化计算a, b

import numpy as np

class SimpleLinearRegression2:

def __init__(self):

"""初始化Single Linear Regression模型"""

self.a_ = None

self.b_ = None

def fit(self, x_train, y_train):

"""根据训练数据集X_train, y_train训练Single Linear Regression模型"""

assert x_train.ndim == 1, "Simple Linear Regressor can only solve single feature training data"

assert len(x_train) == len(y_train), "the size of x_train must be equal to the size of y_train"

x_mean = np.mean(x_train)

y_mean = np.mean(y_train)

num = (x_train - x_mean).dot(y_train - y_mean)

d = (x_train - x_mean).dot(x_train - x_mean)

self.a_ = num / d

self.b_ = y_mean - self.a_ * x_mean

def predict(self, x_predict):

"""给定待测数据集X_predict,返回表示x_predict的结果向量"""

assert x_predict.ndim == 1, "Simple Linear Regressor can only solve single feature training data"

assert self.a_ is not None and self.b_ is not None, "must fit before predict"

return [self._predict(x) for x in x_predict]

def _predict(self, x_single):

"""给定单个待预测数据s_single,返回x_single的预测结果"""

return self.a_ * x_single + self.b_

def __repr__(self):

return "SimpleLinearRegression2()"

绘制结果

import numpy as np

import matplotlib.pyplot as plt

x = np.array([1., 2., 3., 4., 5.])

y = np.array([1., 3., 2., 3., 5.])

reg2 = SimpleLinearRegression2()

reg2.fit(x, y)

y_hat2 = reg2.predict(x)

plt.scatter(x, y)

plt.plot(x, y_hat2, color='r')

plt.axis([0, 6, 0, 6])

plt.show()

输出结果:

向量化实现的性能测试

m = 1000000

big_x = np.random.random(size = m)

big_y = big_x * 3.0 + 2.0 + np.random.normal(size = m)

%timeit reg1.fit(big_x, big_y) # reg1见5-4

%timeit reg2.fit(big_x, big_y)

输出结果:

1.15 s ± 12.7 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

25.2 ms ± 2.08 ms per loop (mean ± std. dev. of 7 runs, 10 loops each)

可见向量化计算能大幅度地提高性能,因此能用向量化计算的地方尽量用向量化计算

分类问题使用accuracy来评价分类结果。

回归问题怎样评价预测结果?

MSE RMSE MAE

均方误差 MSE Mean Squared Error

问题:量纲

均方根误差 RMSE Root Mean Squared Error

与MSE本质上是一样的

与MSE本质上是一样的

放大了最大的错误

平均绝对误差 MAE Mean Absolute Error

训练过程中,没有把这个函数定义成目标函数,是因为它不是处处可导。

但它仍可以用于评价算法

评价一个算法所使用的标准可以和训练时所用的标准不同

编程实现三种

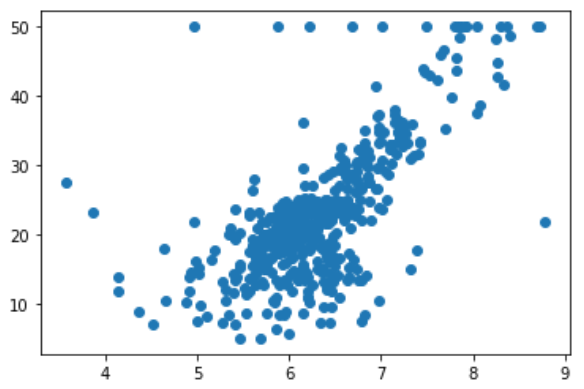

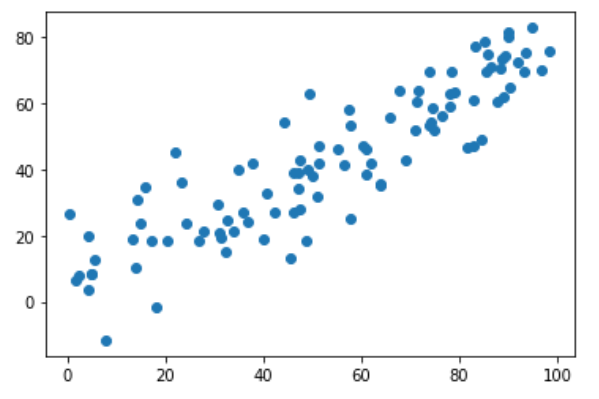

波士顿房产数据

import numpy as np

import matplotlib.pyplot as plt

from sklearn import datasets

boston = datasets.load_boston()

x = boston.data[:, 5] # 5代码房间数,保使用房间数量这个特征

y = boston.target

plt.scatter(x, y)

plt.show()

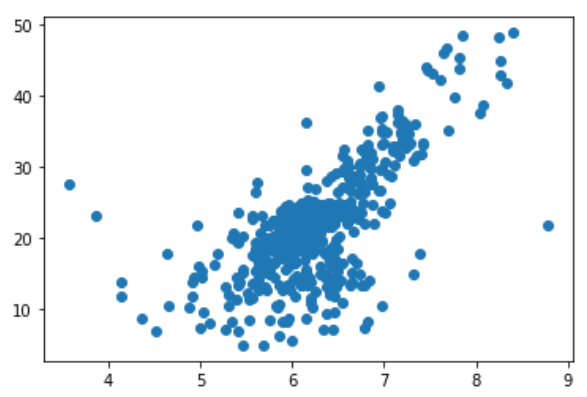

图中最上面有一排点比较奇怪,把它们去掉

x = x[y < 50.0]

y = y[y < 50.0]

plt.scatter(x, y)

plt.show()

训练模型,预测结果

from sklearn.model_selection import train_test_split

x_train, x_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=666)

reg = SimpleLinearRegression() #见5-4

reg.fit(x_train, y_train)

plt.scatter(x_train, y_train)

plt.plot(x_train, reg.predict(x_train), color='r')

plt.show()

评价预测效果

y_predict = reg.predict(x_test)

mse_test = np.sum((y_predict - y_test) ** 2) / len(y_test)

from math import sqrt

rmse_test = sqrt(mse_test)

mae_test = np.sum(np.absolute(y_predict-y_test)) / len(y_test)

使用scikit-learn中的MSE和MAE

from sklearn.metrics import mean_squared_error

from sklearn.metrics import mean_absolute_error

mean_squared_error(y_test, y_predict)

mean_absolute_error(y_test, y_predict)

scikit-learn中没有提供RMSE

RMSE vs MAE

量纲相同

RMSE比MSE大

RMSE有放大y_hat与y较大差距的那个值的趋式

让RMSE更小的意义更大

分类问题使用accuracy来评价分类结果。

1最好,0最差。

即使分类的问题不同,也能很容易的比较它们之间的优劣。

但RMSE和MAE无些特性。

解决方法:R Squared

R Squared

$$ R^2 = 1 - \frac {SS_{residual}}{SS_{total}} = 1 - \frac{\sum_i(\hat y^{(i)}- y^{(i)})^2}{\sum_i(\bar y- y^{(i)})^2} $$

说明:

$$SS_{residual}$$: 使用模型预测产生的错误

$$SS_{total}$$: 把所有样本都预测为$$\bar y$$产生的错误

$$\bar y$$:y的平均值

$$\hat y^{(i)}$$:第i个样本的模型预测值

R Squared代表我们的模型拟合住的数据

R Squared的性质:

- R Squared <= 1

- R Squared越大越好。当我们的预测模型不犯任何错误时,R Squared达到最大值1

- 当我们的模型等于基准模型时,R Squared = 0

- 如果R Squared < 0,说明我们的模型还不如基准模型。此时很有可能数据不存在任何线性关系。

R Squared也可以写成这种形式:

其中Var(y)代表方差

其中Var(y)代表方差

编程实现R Squared

继续使用5-4中的数据和训练结果

1 - mean_squared_error(y_test, y_predict)/np.var(y_test)

或

from sklearn.metrics import r2_score

r2_score(y_test, y_predict)

化简结果:

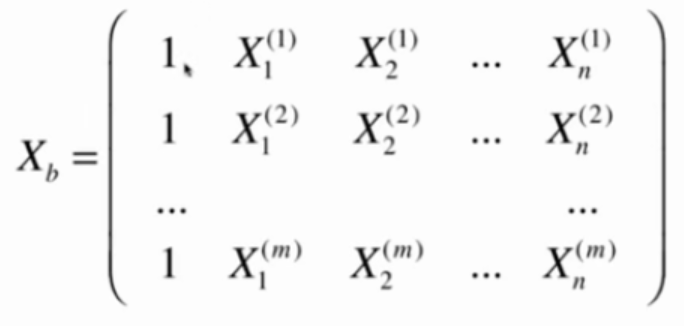

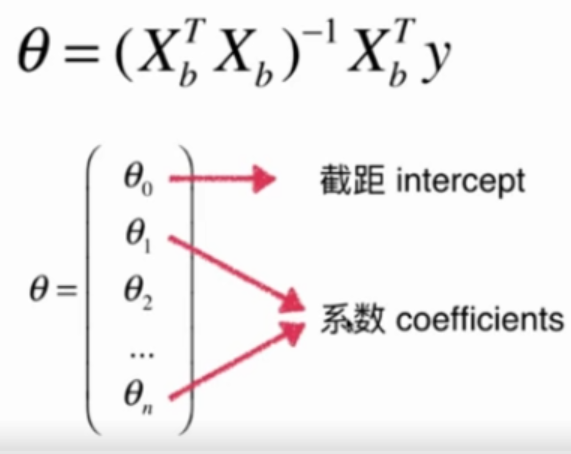

构造矩阵Xb

要使目标函数最小,必须满足

要使目标函数最小,必须满足

直接使用这个公式求解,

缺点:时间复杂度太高,O(n^3)

优点:不需要对数据进行规一化

Linear Regression

import numpy as np

from sklearn.metrics import r2_score

class LinearRegression:

def __init__(self):

"""初始化Linear Regression模型"""

self.coef_ = None

self.interception_ = None

self._theta = None

def fit_normal(self, X_train, y_train):

"""根据训练数据集X_train, y_train训练Linear Regression模型"""

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must be equal to the size of y_train"

X_b = np.hstack([np.ones((len(X_train), 1)), X_train])

self._theta = np.linalg.inv(X_b.T.dot(X_b)).dot(X_b.T).dot(y_train)

self.interception_ = self._theta[0]

self.coef_ = self._theta[1:]

return self

def predict(self, X_predict):

"""给定待预测数据集X_predict,返回表示X_predict的结果向量"""

assert self.interception_ is not None and self.coef_ is not None, "must fit before predict"

assert X_predict.shape[1] == len(self.coef_), "the feature number of X_predict must equal to X_train"

X_b = np.hstack([np.ones((len(X_predict), 1)), X_predict])

return X_b.dot(self._theta)

def score(self, X_test, y_test):

"""根据测试数据集X_test, y_test确定当前模型的准确度"""

y_predict = self.predict(X_test)

return r2_score(y_test, y_predict)

def __repr__(self):

return "LinearRegression()"

boston data

import matplotlib.pyplot as plt

from sklearn import datasets

boston = datasets.load_boston()

x = boston.data

y = boston.target

x = x[y < 50.0]

y = y[y < 50.0]

训练模型与预测结果

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=666)

reg = LinearRegression()

reg.fit_normal(X_train, y_train)

reg.score(X_test, y_test)

输出结果:

0.8129794056212832

使用多个特征训练的模型得分要高于使用单个特征训练的模型

import matplotlib.pyplot as plt

from sklearn import datasets

boston = datasets.load_boston()

x = boston.data

y = boston.target

x = x[y < 50.0]

y = y[y < 50.0]

Linear Regression

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=666)

from sklearn.linear_model import LinearRegression

lin_reg = LinearRegression()

lin_reg.fit(X_train, y_train)

lin_reg.score(X_test, y_test)

KNN Regressor

默认算法

from sklearn.neighbors import KNeighborsRegressor

knn_reg = KNeighborsRegressor()

knn_reg.fit(X_train, y_train)

knn_reg.score(X_test, y_test)

网络搜索

from sklearn.neighbors import KNeighborsRegressor

from sklearn.model_selection import GridSearchCV

param_grid = [

{

'weights':['uniform'],

'n_neighbors': [i for i in range(1, 11)]

},

{

'weights':['distance'],

'n_neighbors': [i for i in range(1, 11)],

'p': [i for i in range(1, 6)]

}

]

knn_reg = KNeighborsRegressor()

grid_search = GridSearchCV(knn_reg, param_grid, n_jobs=-1, verbose=1)

grid_search.fit(X_train, y_train)

输入:grid_search.best_params_

输出:{'n_neighbors': 5, 'p': 1, 'weights': 'distance'}

输入:grid_search.best_score_

输出:0.6340477954176972

输入:grid_search.best_estimator_.score(X_test, y_test)

输出:0.7044357727037996

import matplotlib.pyplot as plt

from sklearn import datasets

boston = datasets.load_boston()

X = boston.data

y = boston.target

X = X[y < 50.0]

y = y[y < 50.0]

from sklearn.linear_model import LinearRegression

lin_reg = LinearRegression()

lin_reg.fit(X, y)

lin_reg.coef_

输出结果:

怎么解释这些数字?

- 系数的正负代表这个特征与房价是正相关还是负相关

- 系数的绝对值大小代码这个特征对房价的影响程度

输入:boston.feature_names[np.argsort(lin_reg.coef_)]

输出:

array(['NOX', 'DIS', 'PTRATIO', 'LSTAT', 'CRIM', 'INDUS', 'AGE', 'TAX',

'B', 'ZN', 'RAD', 'CHAS', 'RM'], dtype='<U7')

即使使用线性回归法预测的模型不够好,观察的它的系数对分析问题也是有帮助的。

线性回归算法的总结

| 线性回归算法 | KNN算法

--|---|--

模型参数 | 典型的参数学习 | 非参数学习

分类问题 | 是很多分类算法的基础 | 可以解决分类问题

回归问题 | 只能解决回归问题 | 可以解决回归问题

对数据的假设性 | 有 | 没有

对数据的解释性 | 有 | 没有

时间复杂度 | 使用正规方程解,在训练模型时复杂度高。

解决方法:梯度下降下 | 预测时复杂度高

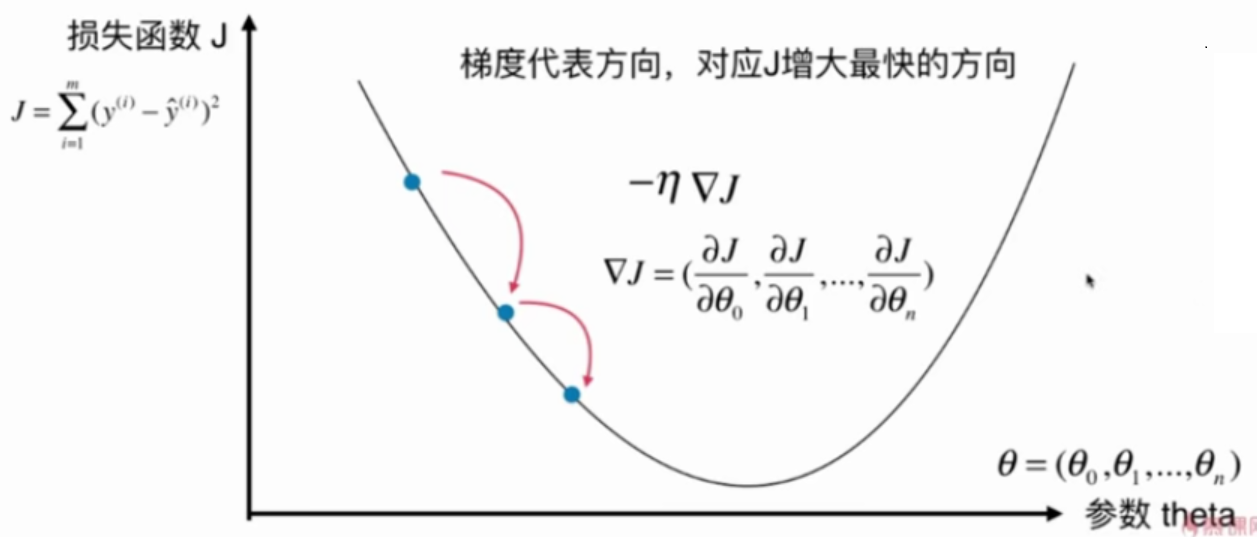

不是一个机器学习算法

是一种基于搜索的最优化算法

作用:最小化一个损失函数

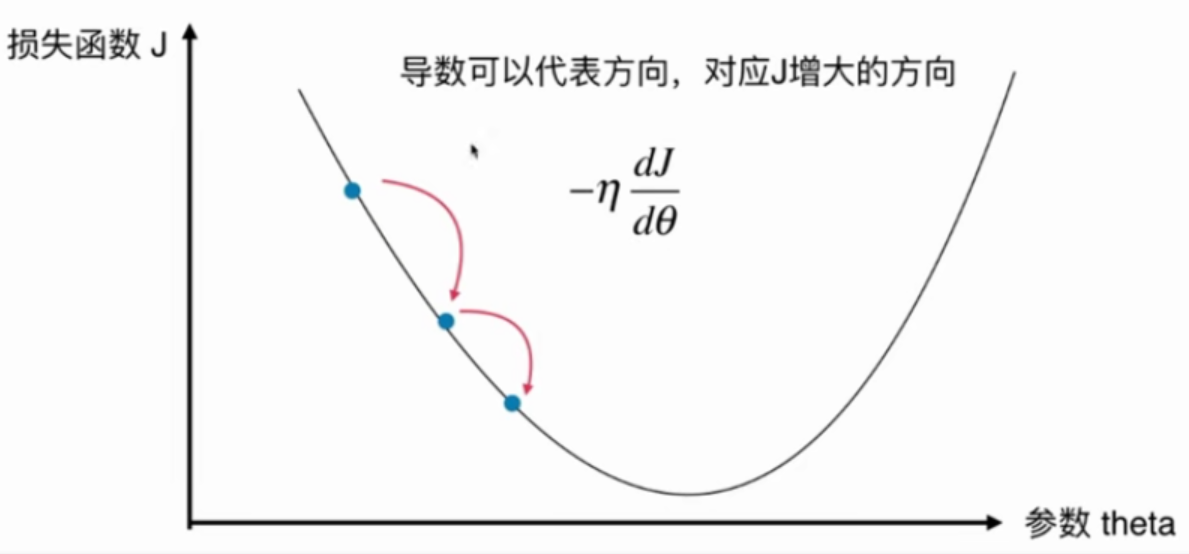

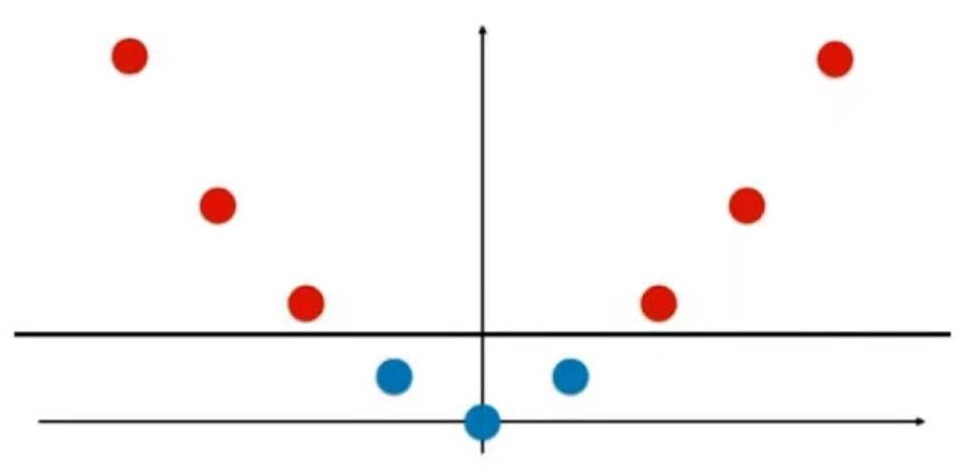

这个二维平面与前面提到的所有二维平面不同。注意坐标系是什么。

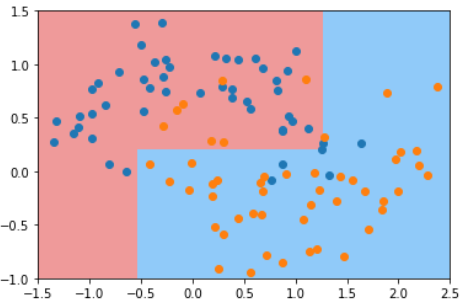

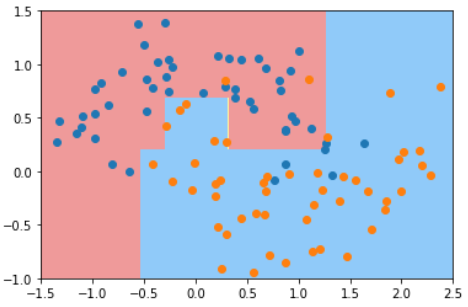

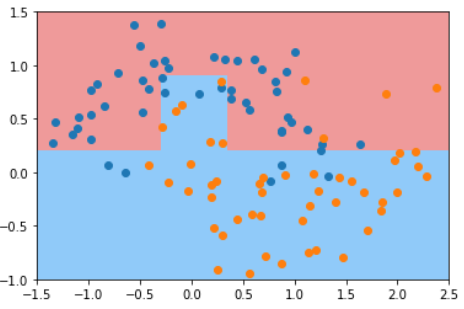

在直线方程中,导数代表斜率

在曲线方程中,导数代表切线斜率

在梯度下降法中,导数代表theta单位变化时,J相应的变化

导数可以代表方向,对应J增大的方向

在梯度下降法中,theta应该向导数的负方向移动

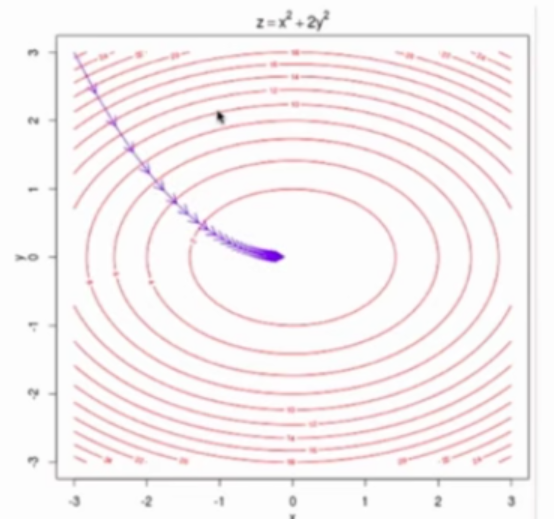

在多维函数中,要对各个方向的分量分别求导,最终得到的方向就是梯度。

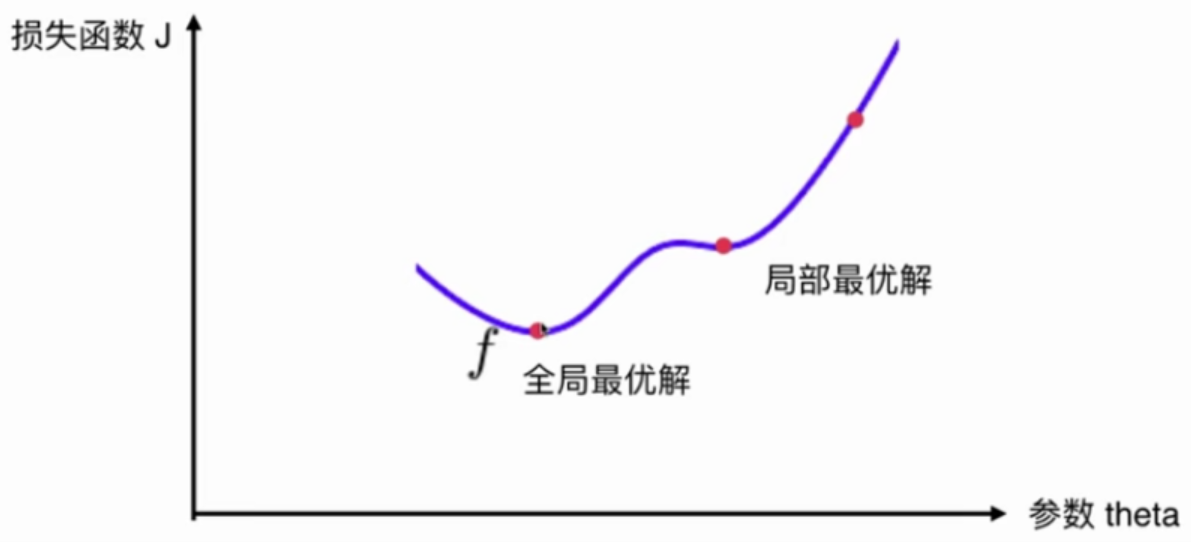

注意:并不是所有函数都有唯一的极值点

解决方法:

多次运行,随机化初始化点

梯度下降法的初始点也是一个超参数

线性回归问题,损失函数J具有唯一最优解

不是一个机器学习算法

是一种基于搜索的最优化算法

作用:最小化一个损失函数

这个二维平面与前面提到的所有二维平面不同。注意坐标系是什么。

在直线方程中,导数代表斜率

在曲线方程中,导数代表切线斜率

在梯度下降法中,导数代表theta单位变化时,J相应的变化

导数可以代表方向,对应J增大的方向

在梯度下降法中,theta应该向导数的负方向移动

在多维函数中,要对各个方向的分量分别求导,最终得到的方向就是梯度。

注意:并不是所有函数都有唯一的极值点

解决方法:

多次运行,随机化初始化点

梯度下降法的初始点也是一个超参数

线性回归问题,损失函数J具有唯一最优解

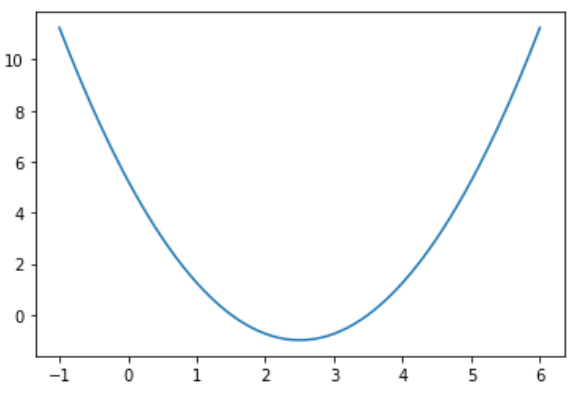

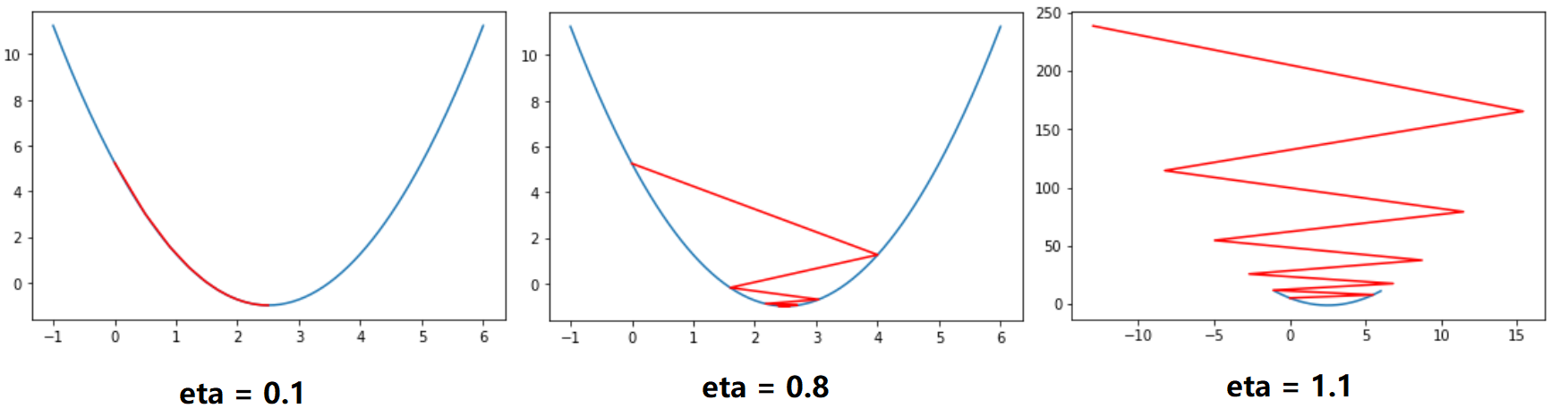

假设损失函数J是这样的:

import numpy as np

import matplotlib.pyplot as plt

plot_x = np.linspace(-1, 6, 141)

plot_y = (plot_x - 2.5) ** 2 -1

plt.plot(plot_x, plot_y)

plt.show()

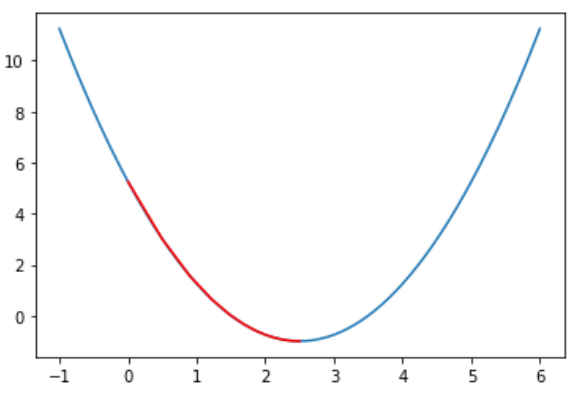

梯度下降算法实现

def dJ(theta):

return 2*(theta - 2.5)

def J(theta):

return (theta-2.5) ** 2 -1

eta = 0.1

epsilon = 1e-8

theta = 0

while True:

gradient = dJ(theta)

last_theta = theta

theta = theta - eta * gradient

if (abs(J(theta) - J(last_theta)) < epsilon):

break

print (theta)

print (J(theta))

输出结果:

2.499891109642585

-0.99999998814289

在图是显示所有的theta的轨迹

def gradient_descent(initial_theta, eta, epsilon=1e-8):

theta = initial_theta

theta_history = [theta]

while True:

gradient = dJ(theta)

last_theta = theta

theta = theta - eta * gradient

theta_history.append(theta)

#print (theta)

if (abs(J(theta) - J(last_theta)) < epsilon):

break

return theta_history

def plot_theta_history():

plt.plot(plot_x, J(plot_x))

plt.plot(np.array(theta_history), J(np.array(theta_history)), color='r')

plt.show()

eta = 0.01

theta_history = gradient_descent(0., eta)

plot_theta_history()

输出结果:

eta取不同参数的绘制结果

def gradient_descent(initial_theta, eta, n_iters = 10, epsilon=1e-8):

theta = initial_theta

theta_history = [theta]

i_iter = 0

while i_iter < n_iters:

gradient = dJ(theta)

last_theta = theta

theta = theta - eta * gradient

theta_history.append(theta)

print (theta)

if (abs(J(theta) - J(last_theta)) < epsilon):

break

i_iter += 1

return theta_history

输出结果:

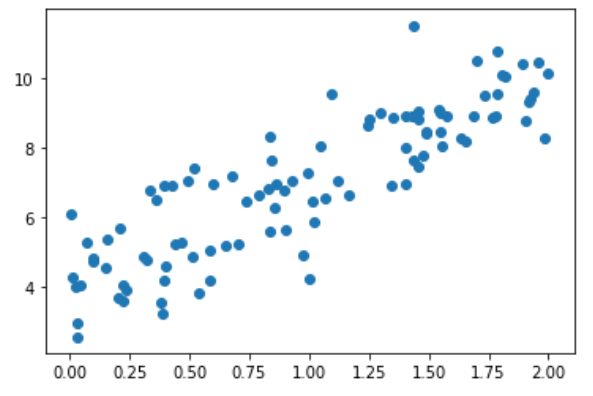

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(666)

x = 2 * np.random.random(size=100)

y = x * 3. + 4. + np.random.normal(size=100)

X = x.reshape(-1, 1)

plt.scatter(x, y)

plt.show()

使用梯度下降法训练

def J(theta, X_b, y):

try:

return np.sum((y - X_b.dot(theta))**2) / len(X_b)

except:

return float('inf')

def dJ(theta, X_b, y):

ret = np.empty(len(theta))

ret[0] = np.sum(X_b.dot(theta) - y)

for i in range(1, len(theta)):

ret[i] = (X_b.dot(theta) - y).dot(X_b[:, 1])

return ret * 2 / len(X_b)

def gradient_descent(X_b, y, initial_theta, eta, n_iters = 1e4, epsilon=1e-8):

theta = initial_theta

i_iter = 0

while i_iter < n_iters:

gradient = dJ(theta, X_b, y)

last_theta = theta

theta = theta - eta * gradient

if (abs(J(theta, X_b, y) - J(last_theta, X_b, y)) < epsilon):

break

i_iter += 1

return theta

X_b = np.hstack([np.ones((len(x), 1)), X])

initial_theta = np.zeros(X_b.shape[1])

eta = 0.01

theta = gradient_descent(X_b, y, initial_theta, eta)

theta

输出结果:

array([4.02145786, 3.00706277])

封装线性回归算法

import numpy as np

from sklearn.metrics import r2_score

class LinearRegression:

def __init__(self):

"""初始化Linear Regression模型"""

self.coef_ = None

self.interception_ = None

self._theta = None

def fit_normal(self, X_train, y_train):

"""根据训练数据集X_train, y_train训练Linear Regression模型"""

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must be equal to the size of y_train"

X_b = np.hstack([np.ones((len(X_train), 1)), X_train])

self._theta = np.linalg.inv(X_b.T.dot(X_b)).dot(X_b.T).dot(y_train)

self.interception_ = self._theta[0]

self.coef_ = self._theta[1:]

return self

def fit_gd(self, X_train, y_train, eta=0.01, n_iters = 1e4):

"""根据训练数据集X_train, y_train,使用梯度下降法训练Linear Regression模型"""

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must be equal to the size of y_train"

def J(theta, X_b, y):

try:

return np.sum((y - X_b.dot(theta))**2) / len(X_b)

except:

return float('inf')

def dJ(theta, X_b, y):

ret = np.empty(len(theta))

ret[0] = np.sum(X_b.dot(theta) - y)

for i in range(1, len(theta)):

ret[i] = (X_b.dot(theta) - y).dot(X_b[:, 1])

return ret * 2 / len(X_b)

def gradient_descent(X_b, y, initial_theta, eta, n_iters = 1e4, epsilon=1e-8):

theta = initial_theta

i_iter = 0

while i_iter < n_iters:

gradient = dJ(theta, X_b, y)

last_theta = theta

theta = theta - eta * gradient

if (abs(J(theta, X_b, y) - J(last_theta, X_b, y)) < epsilon):

break

i_iter += 1

return theta

X_b = np.hstack([np.ones((len(X_train), 1)), X_train])

initial_theta = np.zeros(X_b.shape[1])

self._theta = gradient_descent(X_b, y_train, initial_theta, eta)

self.interception_ = self._theta[0]

self.coef_ = self._theta[1:]

return self

def predict(self, X_predict):

"""给定待预测数据集X_predict,返回表示X_predict的结果向量"""

assert self.interception_ is not None and self.coef_ is not None, "must fit before predict"

assert X_predict.shape[1] == len(self.coef_), "the feature number of X_predict must equal to X_train"

X_b = np.hstack([np.ones((len(X_predict), 1)), X_predict])

return X_b.dot(self._theta)

def score(self, X_test, y_test):

"""根据测试数据集X_test, y_test确定当前模型的准确度"""

y_predict = self.predict(X_test)

return r2_score(y_test, y_predict)

def __repr__(self):

return "LinearRegression()"

使用fit_gd

lin_reg = LinearRegression()

lin_reg.fit_gd(X, y)

输入:lin_reg.coef_

输出:array([3.00706277])

输入:lin_reg.interception_

输出:4.021457858204859

测试数据

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(666)

x = 2 * np.random.random(size=100)

y = x * 3. + 4. + np.random.normal(size=100)

X = x.reshape(-1, 1)

plt.scatter(x, y)

plt.show()

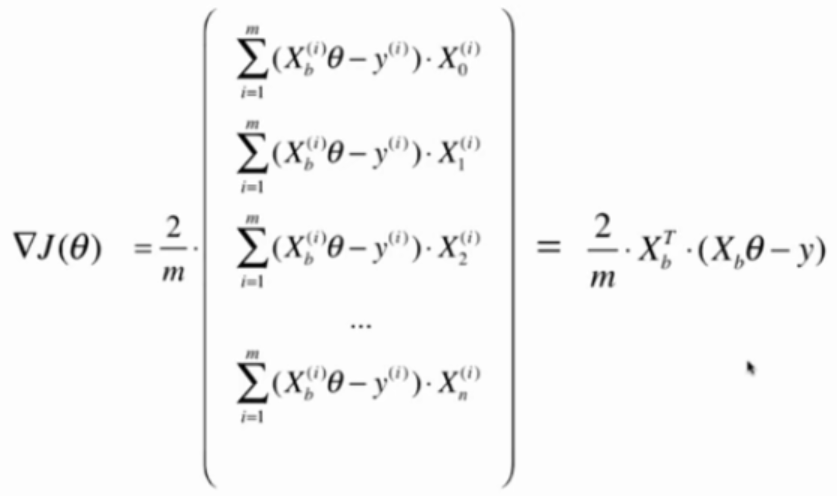

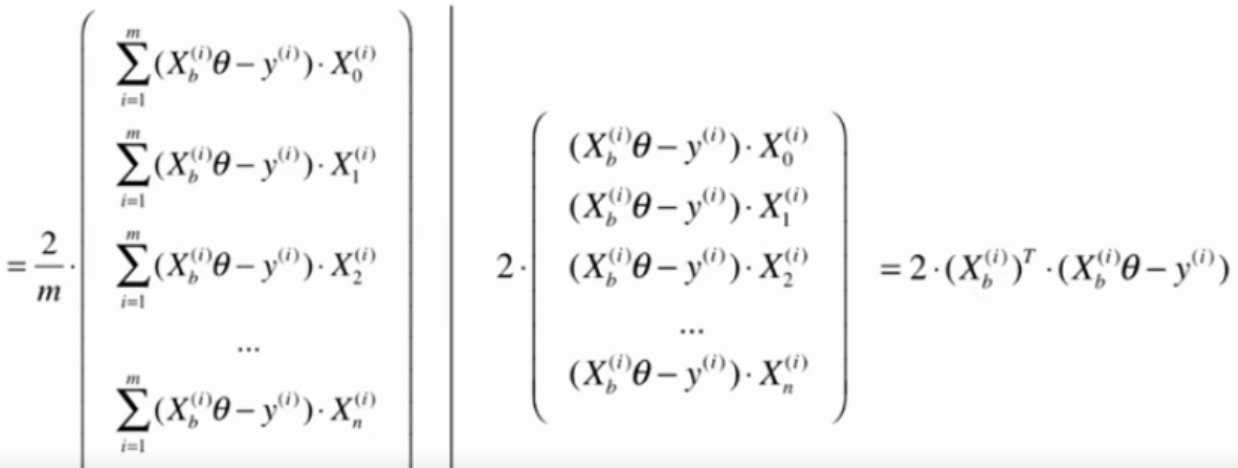

向量化计算dJ

def dJ(theta, X_b, y):

return X_b.T.dot(X_b.dot(theta)-y) * 2. / len(X_b)

使用真实数据测试模型

真实数据 + 正规化方程解

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=666)

lin_reg1 = LinearRegression()

lin_reg1.fit_normal(X_train, y_train) # 见5-4

lin_reg1.score(X_test, y_test)

输出结果:

0.8129794056212832

真实数据 + 梯度下降法

lin_reg2 = LinearRegression()

lin_reg2.fit_gd(X_train, y_train)

lin_reg2.score(X_test, y_test)

输出结果:

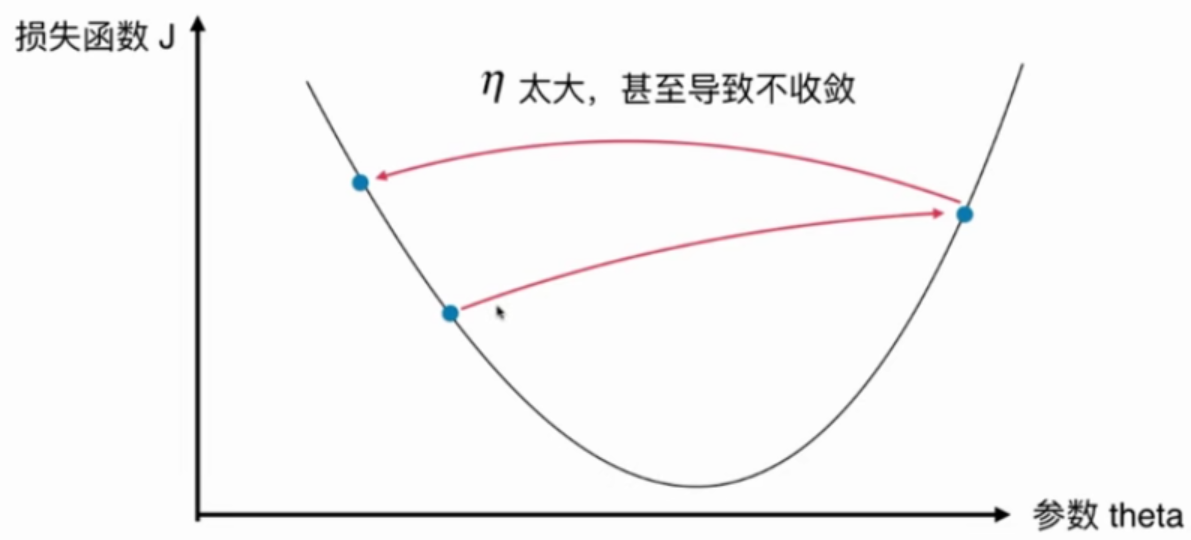

eta太大导致搜索过程不收敛

真实数据 + 梯度下降法 + eta=0.000001

lin_reg2 = LinearRegression()

lin_reg2.fit_gd(X_train, y_train, eta = 0.000001)

lin_reg2.score(X_test, y_test)

输出结果:

0.27586818724477247

训练次数不够,没有达到最优值

真实数据 + 梯度下降法 + eta=0.000001 + n_iters=1e6

lin_reg2 = LinearRegression()

lin_reg2.fit_gd(X_train, y_train, eta = 0.000001, n_iters=1e6)

lin_reg2.score(X_test, y_test)

输出结果:

0.7542932581943915

训练次数太多,导致训练时间太长,但次数又不足以找到最优解

解决方法:数据归一化

梯度下降法与数据归一化

多元线性回归问题中,不同特征的规格一样,导致eta很难选。同一个eta可能会导致某些无法收敛而另一特征又收敛太慢。

因此使用梯度下降法之前,最好对数据进行归一化

from sklearn.preprocessing import StandardScaler

standardScaler = StandardScaler()

standardScaler.fit(X_train)

X_train_standard = standardScaler.transform(X_train)

X_test_standard = standardScaler.transform(X_test)

lin_reg3 = LinearRegression()

lin_reg3.fit_gd(X_train_standard, y_train)

lin_reg3.score(X_test_standard, y_test)

输出结果:

0.8129873310487505

常规的梯度下降法,又叫批量梯度下降法,Batch Gradient Descent

问题:当样本数m很大时会非常耗时

解决方法:每次只对其中一个样本做计算

把去掉m后计算的公式作为搜索的方向。

由于不能保证这种方法计算得到的方向一定是损失最小的方向,甚至不能保证一定是损失函数减小的方向。也不能找到最小值的位置。

但仍然能到函数的最小值附近。

如果m非常大,可以用一定的精度来换时间。

在随机梯度下降法过程中,学习率很重要。

如果学习率取固定值,很有可以到了最小值附近后又跳出去了。

学习率应逐渐递减。(模拟退火的思想)

通常a取5,b取50

测试数据

import numpy as np

import matplotlib.pyplot as plt

m = 100000

x = np.random.normal(size=m)

X = x.reshape(-1, 1)

y = 4. * x + 3. + np.random.normal(0, 3, size=m)

批量梯度下降法

算法

def J(theta, X_b, y):

try:

return np.sum((y - X_b.dot(theta))**2) / len(X_b)

except:

return float('inf')

def dJ(theta, X_b, y):

return X_b.T.dot(X_b.dot(theta)-y) * 2. / len(X_b)

def gradient_descent(X_b, y, initial_theta, eta, n_iters = 1e4, epsilon=1e-8):

theta = initial_theta

i_iter = 0

while i_iter < n_iters:

gradient = dJ(theta, X_b, y)

last_theta = theta

theta = theta - eta * gradient

if (abs(J(theta, X_b, y) - J(last_theta, X_b, y)) < epsilon):

break

i_iter += 1

return theta

测试性能

%%time

X_b = np.hstack([np.ones((len(X), 1)), X])

initial_theta = np.zeros(X_b.shape[1])

eta = 0.01

theta = gradient_descent(X_b, y, initial_theta, eta)

耗时:2s

theta = array([3.00456203, 3.98777265])

随机梯度下降法

算法

def J(theta, X_b, y):

try:

return np.sum((y - X_b.dot(theta))**2) / len(X_b)

except:

return float('inf')

def dJ_sgd(theta, X_b_i, y_i):

return X_b_i.T.dot(X_b_i.dot(theta)-y_i) * 2.

def sgd(X_b, y, initial_theta, n_iters):

t0 = 5

t1 = 50

def learning_rate(t):

return t0 / (t + t1)

theta = initial_theta

i_iter = 0

for i_iter in range (n_iters):

rand_i = np.random.randint(len(X_b))

gradient = dJ_sgd(theta, X_b[rand_i], y[rand_i])

last_theta = theta

theta = theta - learning_rate(i_iter) * gradient

# 不能保证梯度一直是减小的

# if (abs(J(theta, X_b, y) - J(last_theta, X_b, y)) < epsilon):

# break

return theta

测试性能

%%time

X_b = np.hstack([np.ones((len(X), 1)), X])

initial_theta = np.zeros(X_b.shape[1])

theta = sgd(X_b, y, initial_theta, n_iters=len(X_b)//3) # 这里只检查了1/3样本,对于多元线性回归问题不能这样

耗时:471ms

array([2.94954458, 3.95898273])

时间大幅度减少而结果和批量梯度下降法差不多。

当m特别大时,可以牺牲一定的精度来换取时间。

import numpy as np

from sklearn.metrics import r2_score

class LinearRegression:

def __init__(self):

"""初始化Linear Regression模型"""

self.coef_ = None

self.interception_ = None

self._theta = None

def fit_normal(self, X_train, y_train):

"""根据训练数据集X_train, y_train训练Linear Regression模型"""

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must be equal to the size of y_train"

X_b = np.hstack([np.ones((len(X_train), 1)), X_train])

self._theta = np.linalg.inv(X_b.T.dot(X_b)).dot(X_b.T).dot(y_train)

self.interception_ = self._theta[0]

self.coef_ = self._theta[1:]

return self

def fit_gd(self, X_train, y_train, eta=0.01, n_iters = 1e4):

"""根据训练数据集X_train, y_train,使用梯度下降法训练Linear Regression模型"""

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must be equal to the size of y_train"

def J(theta, X_b, y):

try:

return np.sum((y - X_b.dot(theta))**2) / len(X_b)

except:

return float('inf')

def dJ(theta, X_b, y):

return X_b.T.dot(X_b.dot(theta)-y) * 2. / len(X_b)

def gradient_descent(X_b, y, initial_theta, eta, n_iters = 1e4, epsilon=1e-8):

theta = initial_theta

i_iter = 0

while i_iter < n_iters:

gradient = dJ(theta, X_b, y)

last_theta = theta

theta = theta - eta * gradient

if (abs(J(theta, X_b, y) - J(last_theta, X_b, y)) < epsilon):

break

i_iter += 1

return theta

X_b = np.hstack([np.ones((len(X_train), 1)), X_train])

initial_theta = np.zeros(X_b.shape[1])

self._theta = gradient_descent(X_b, y_train, initial_theta, eta)

self.interception_ = self._theta[0]

self.coef_ = self._theta[1:]

return self

def fit_sgd(self, X_train, y_train, n_iters = 5, t0 = 5, t1 = 50):

"""根据训练数据集X_train, y_train,使用随机梯度下降法训练Linear Regression模型"""

assert X_train.shape[0] == y_train.shape[0], "the size of X_train must be equal to the size of y_train"

def dJ_sgd(theta, X_b_i, y_i):

return X_b_i.T.dot(X_b_i.dot(theta)-y_i) * 2.

def learning_rate(t, t0, t1):

return t0 / (t + t1)

def sgd(X_b, y, initial_theta, n_iters, t0, t1): # n_iters:对所有的样本看几圈

theta = initial_theta

m = len(X_b)

i_iter = 0

for i_iter in range (n_iters):

indexes = np.random.permutation(m)

X_b_new = X_b[indexes]

y_new = y[indexes]

for i in range (m):

gradient = dJ_sgd(theta, X_b_new[i], y_new[i])

last_theta = theta

theta = theta - learning_rate(i_iter*m+i, t0, t1) * gradient

return theta

X_b = np.hstack([np.ones((len(X_train), 1)), X_train])

initial_theta = np.zeros(X_b.shape[1])

self._theta = sgd(X_b, y_train, initial_theta, n_iters, t0, t1)

self.interception_ = self._theta[0]

self.coef_ = self._theta[1:]

return self

def predict(self, X_predict):

"""给定待预测数据集X_predict,返回表示X_predict的结果向量"""

assert self.interception_ is not None and self.coef_ is not None, "must fit before predict"

assert X_predict.shape[1] == len(self.coef_), "the feature number of X_predict must equal to X_train"

X_b = np.hstack([np.ones((len(X_predict), 1)), X_predict])

return X_b.dot(self._theta)

def score(self, X_test, y_test):

"""根据测试数据集X_test, y_test确定当前模型的准确度"""

y_predict = self.predict(X_test)

return r2_score(y_test, y_predict)

def __repr__(self):

return "LinearRegression()"

测试数据 + sgd

m = 100000

x = np.random.normal(size=m)

X = x.reshape(-1, 1)

y = 4. * x + 3. + np.random.normal(0, 3, size=m)

lin_reg = LinearRegression()

lin_reg.fit_sgd(X, y, n_iters=2)

刚开始在代码中犯了个错误,没有把L78的i_iter改成i_iter*m+i,

导致每次训练得到的模型差点都非常大,且偏离正确值也非常大。

改掉之后就好了,

可以如果学习率使用固定值,不能得到很好的效果。

真实数据 + sgd

真实数据

from sklearn import datasets

boston = datasets.load_boston()

X = boston.data

y = boston.target

X = X[y<50.0]

y = y[y<50.0]

预处理

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=666)

from sklearn.preprocessing import StandardScaler

standScaler = StandardScaler()

standScaler.fit(X_train)

X_train_standard = standScaler.transform(X_train)

X_test_standard = standScaler.transform(X_test)

SGD

lin_reg = LinearRegression()

%time lin_reg.fit_sgd(X_train_standard, y_train)

lin_reg.score(X_test_standard, y_test)

n_iters对score和Wall time的影响

| n_iters | score | Wall time |

|---|---|---|

| 5 | 0.7763594773981595 | 30.7 ms |

| 50 | 0.8130771495096732 | 271 ms |

| 100 | 0.8131205440883096 | 462 ms |

真实数据 + sklearn的SGD

from sklearn.linear_model import SGDRegressor

sgd_lin = SGDRegressor()

%time sgd_lin.fit(X_train_standard, y_train)

sgd_lin.score(X_test_standard, y_test)

模型的得分差不多,但sklearn的SGD的速度明显快很多。

因为sklearn的SGD的实现过程与课程中有很大的不同。

视频还测试了SGDRegressor的n_iter参数。

这个参数在我用的sklearn版本中已经没有了。

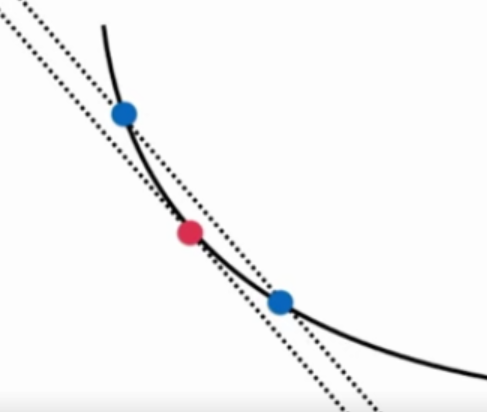

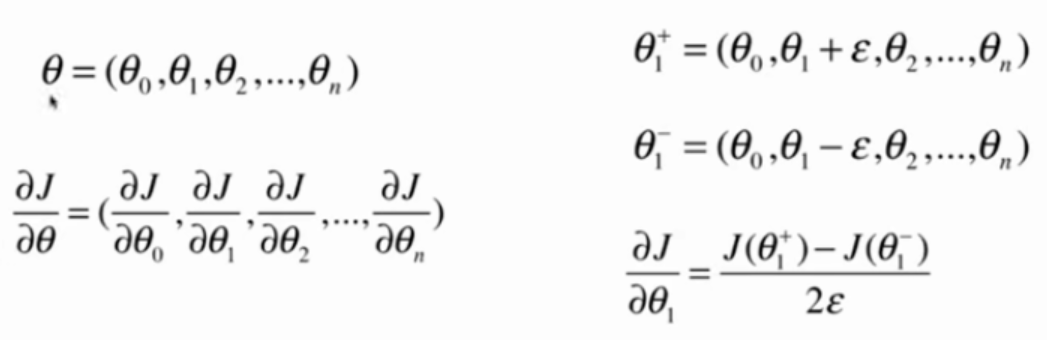

梯度的求解并不容易,如果知道自己求的梯度是否正确?

图中两条直线的斜率近乎相等。

两个蓝点越接近,斜率越相近。

推广到高维场景

代码实现

准备数据

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(666)

X = np.random.random(size=(1000, 10))

true_theta = np.arange(1, 12, dtype=float)

X_b = np.hstack([np.ones((len(X), 1)), X])

y = X_b.dot(true_theta) + np.random.normal(size=1000)

def J(theta, X_b, y):

try:

return np.sum((y - X_b.dot(theta))**2) / len(X_b)

except:

return float('inf')

两种方法求导数

def dJ_math(theta, X_b, y):

return X_b.T.dot(X_b.dot(theta) - y) * 2. / len(y)

def dJ_debug(theta, X_b, y, epsilon=0.01):

ret = np.empty(len(theta))

for i in range(len(theta)):

theta_1 = theta.copy()

theta_1[i] +=epsilon

theta_2 = theta.copy()

theta_2[i] -=epsilon

ret[i] = (J(theta_1, X_b, y) - J(theta_2, X_b, y)) / (2*epsilon)

return ret

两种方法训练模型

def gradient_descent(dJ, X_b, y, initial_theta, eta, n_iters = 1e4, epsilon=1e-8):

theta = initial_theta

i_iter = 0

while i_iter < n_iters:

gradient = dJ(theta, X_b, y)

last_theta = theta

theta = theta - eta * gradient

if (abs(J(theta, X_b, y) - J(last_theta, X_b, y)) < epsilon):

break

i_iter += 1

return theta

X_b = np.hstack([np.ones((len(X), 1)), X])

initial_theta = np.zeros(X_b.shape[1])

eta = 0.01

%time theta = gradient_descent(dJ_debug, X_b, y, initial_theta, eta)

%time theta = gradient_descent(dJ_math, X_b, y, initial_theta, eta)

实验结果

dJ_math对应的运行时间为:660 ms

dJ_debug对应的运行时间为:4.58s

两种方法求出的theta完全相同

dJ_debug的方法可以用于求梯度,最终能得到正确的结果

dJ_debug速度很慢。

可以先使用dJ_debug得到想要的正确结果。

再用dJ_math将得到的结果与dJ_debug的结果相比较,来验证数学是否正确。

dJ_debug与J无关,可以适用于所有函数。

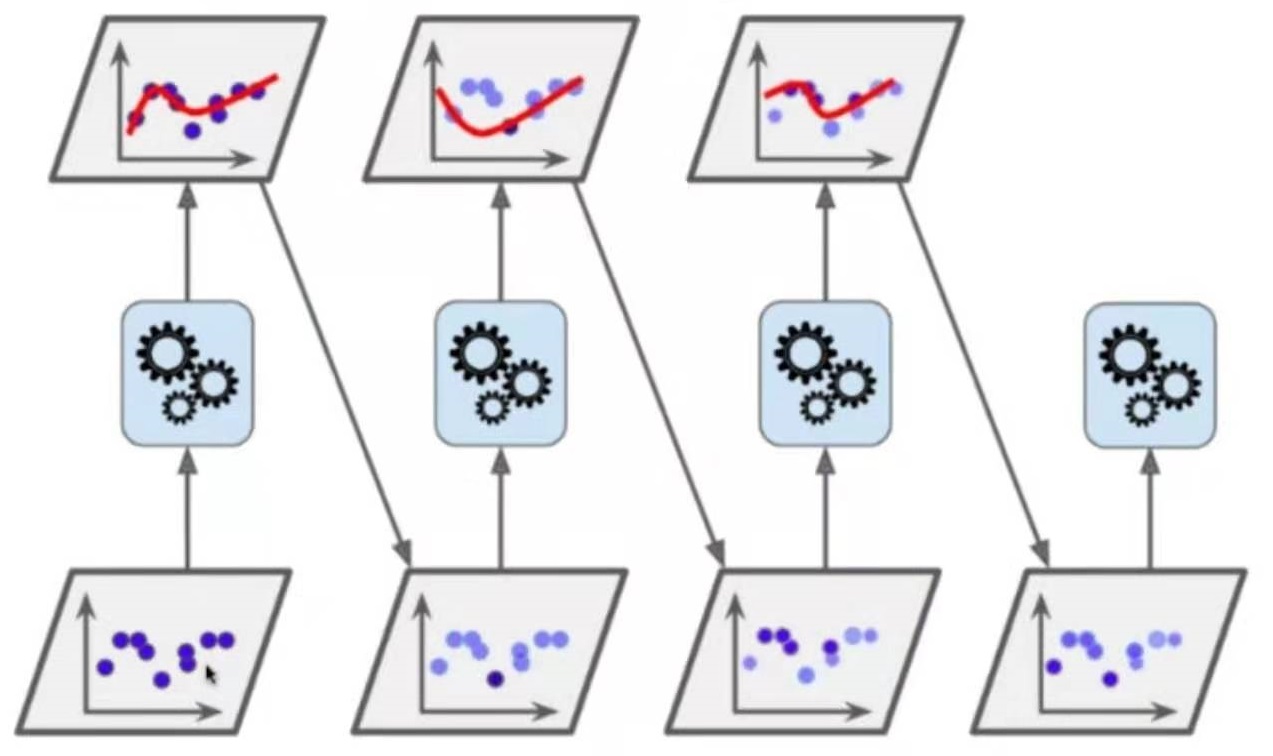

- 批量梯度下降法 Batch Gradient Descent,缺点:慢,优点:稳定

- 随机梯度下降法 Stochastic Gradient Descent,优点:快,缺点:不稳定

- 小批量梯度下降法 Mini-Batch Gradient Descent,以上两种结合

随机

随机梯度下降法可以跳出局部最优解

随机梯度下降法运行速度更快

机器学习领域很多算法都要使用随机的特点,例如随机搜索、随机森林

主成分分析法 PCA Principal Component Analysis

一个非监督的机器学习算法

主要用于数据的降维

通过降维,可以发现更便于人类理解的特征

其他应用:可视化,去噪

主成分分析法 PCA Principal Component Analysis

一个非监督的机器学习算法

主要用于数据的降维

通过降维,可以发现更便于人类理解的特征

其他应用:可视化,去噪

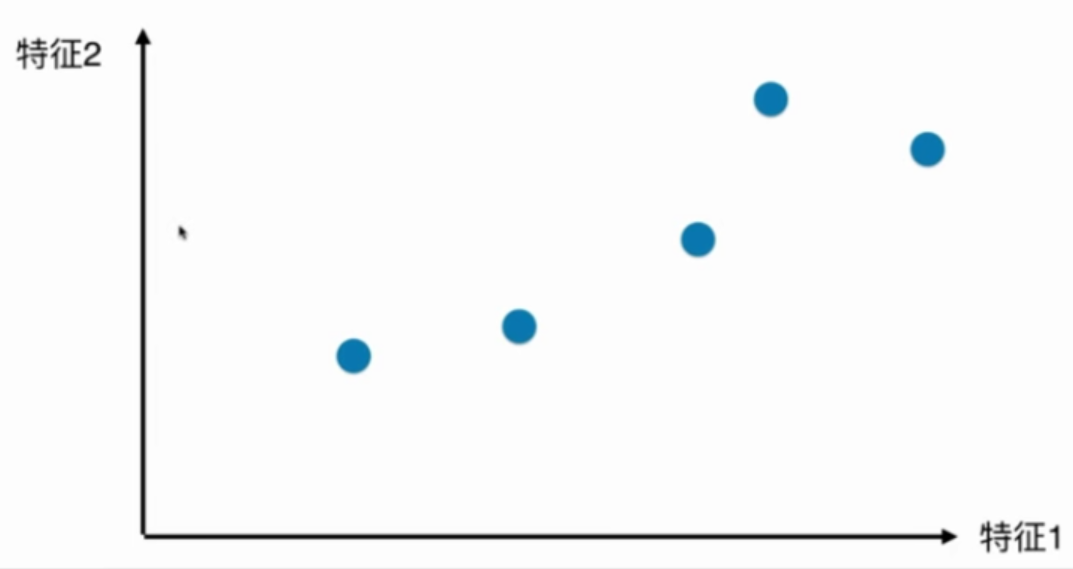

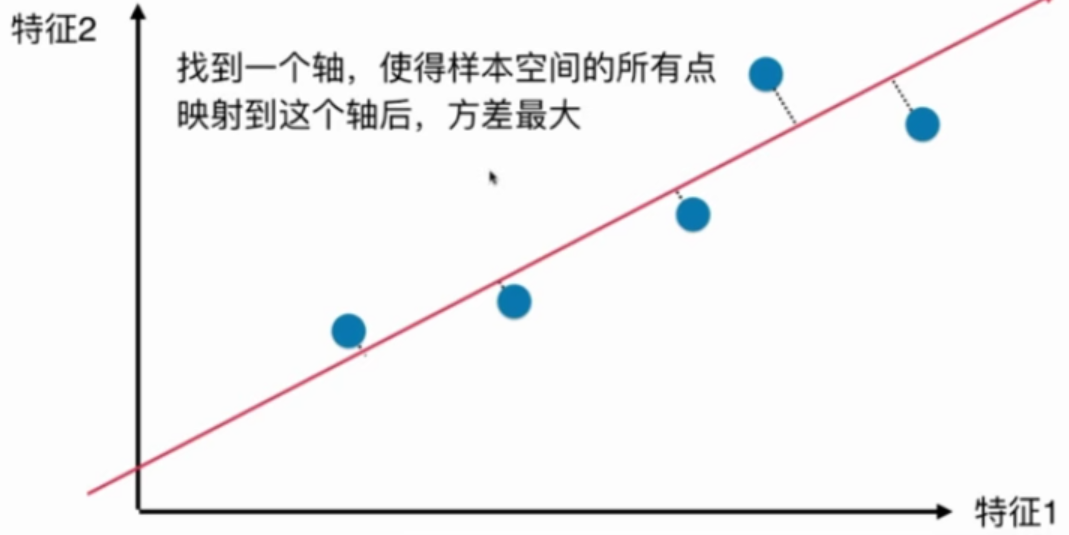

二维降至一维

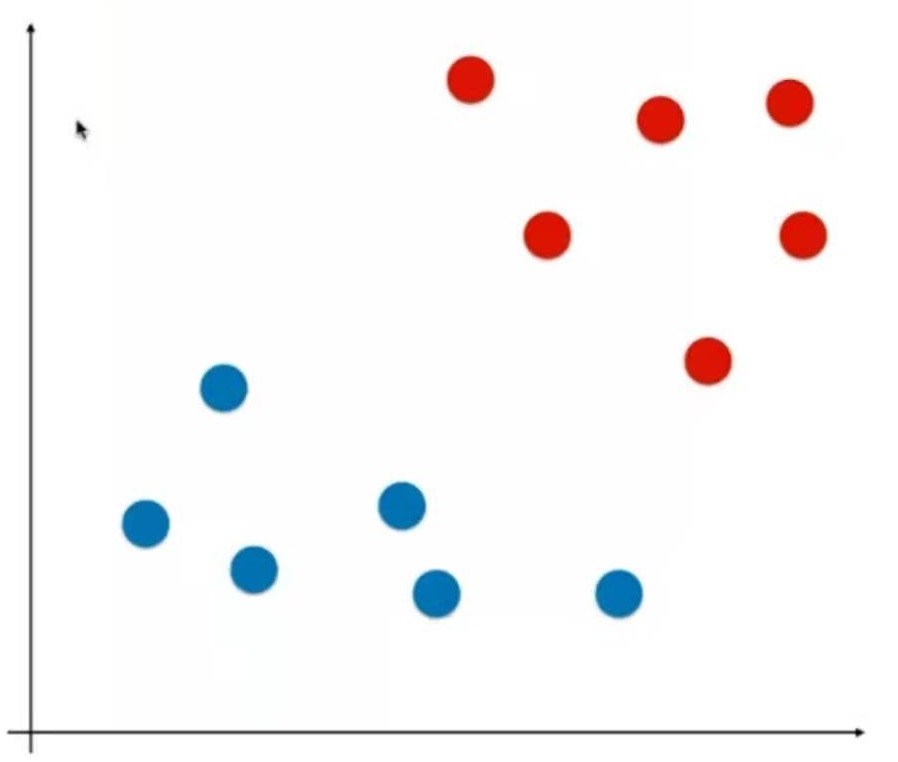

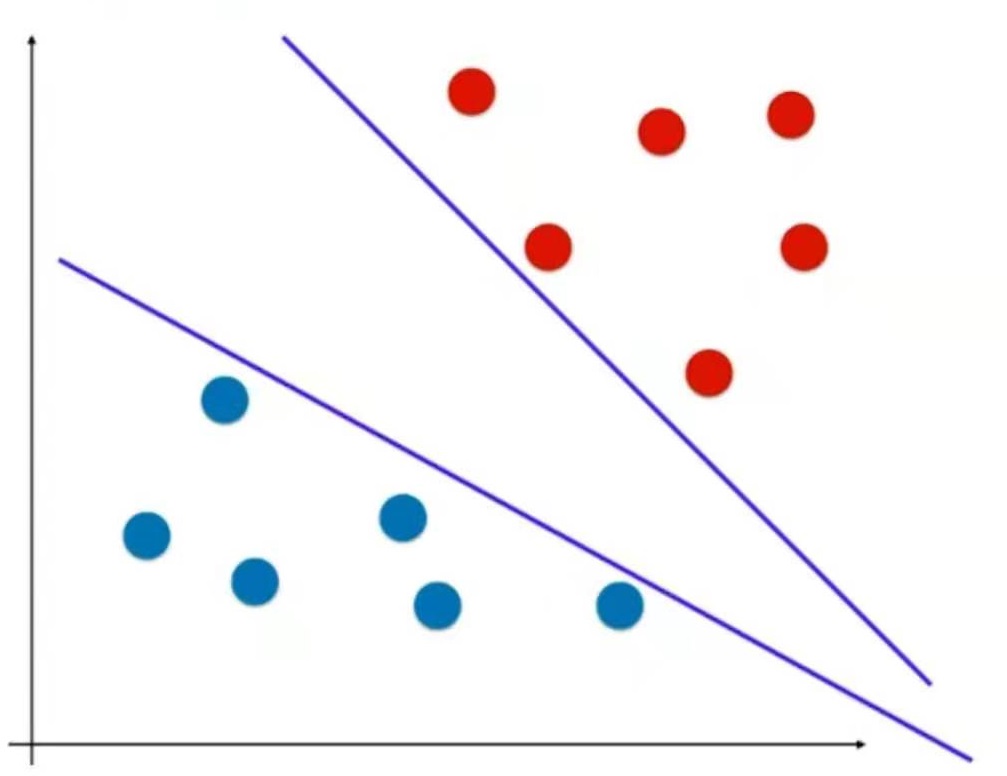

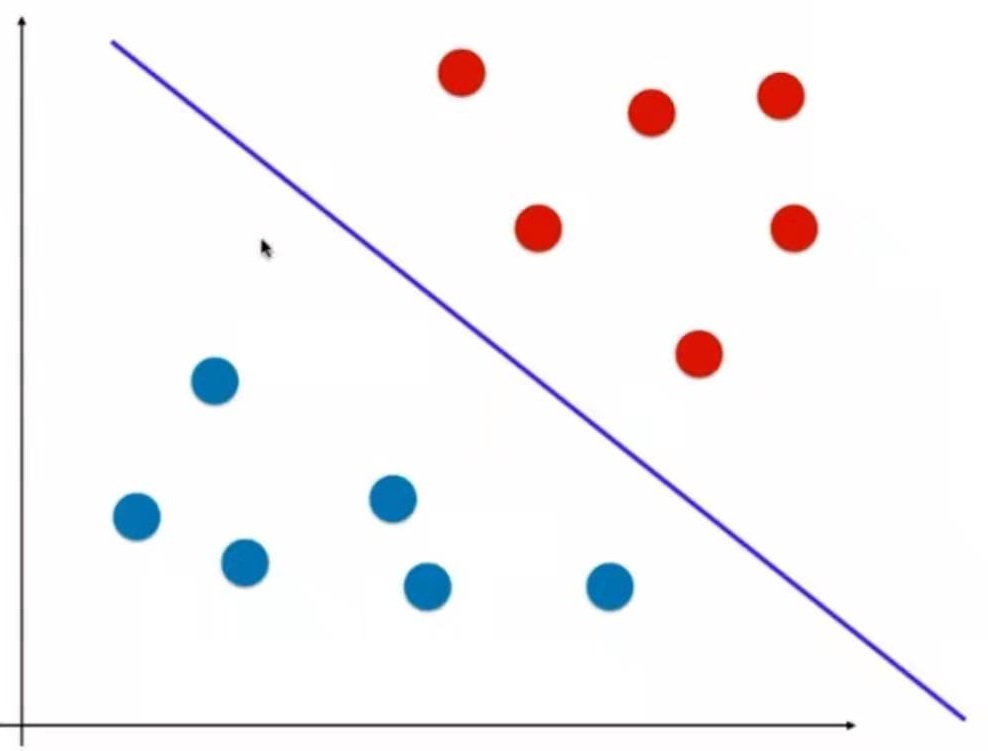

如何把图中的二维空间中的点降至一维?

以上三种方法哪种更好?

第三种,因为第三种最大程度地保留了原数据之间的关系.

概率论与数理统计中, 方差(Variance)描述了样本整体疏密的一个指标.

如何找到这个样本间间距(方差)最大的轴?

$$ \begin{aligned} Var(x) = \frac{1}{m}\sum_{i=1}^m(x_i-\bar x)^2 && (1) \end{aligned} $$

其中 $$\bar x$$ 代表x的平均值。

第一步:将所有样本的均值归0 (demean)

由于均值为0,则公式(1)可以化简为:

$$ \begin{aligned} Var(x) = \frac{1}{m}\sum_{i=1}^m(x_i-\bar x)^2 = \frac{1}{m}\sum_{i=1}^mx_i^2 && (2) \end{aligned} $$

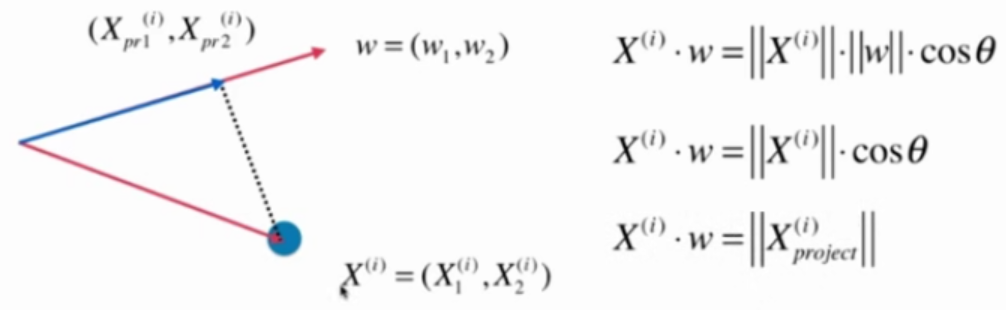

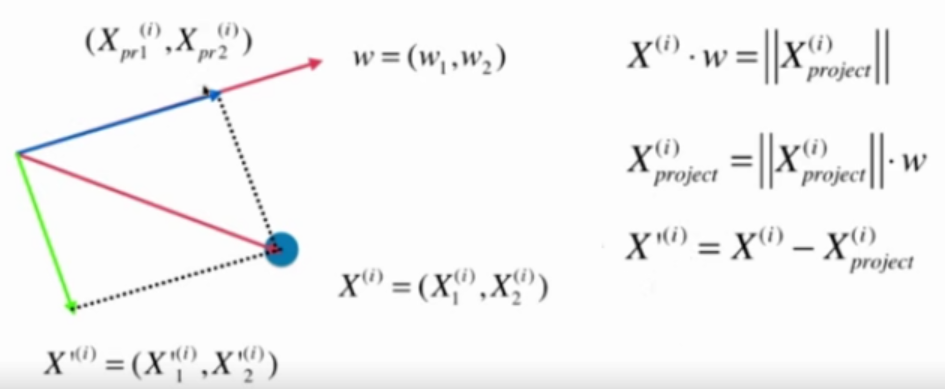

这里的x是样本映射到坐标轴以后的新的样本的值 $$X_{\text{project}}$$ 。

第二步:求一个轴的方向w = (w1, w2),使用所有的样本映射到w以后,有 $$Var(X_{\text{project}})$$ 最大:

$$ \begin{aligned} Var(X_{\text{project}}) = \frac{1}{m}\sum_{i=1}^m||x^{(i)}_{\text{project}}||^2 && (3) \end{aligned} $$

推导过程:

假设均值化之后的x的坐标为

$$ X^{(i)}=(X^{(i)}_1, X^{(i)}_2) $$

要映射的坐标轴为 $$w-{w_1, w_2}$$

$$X^{(i)}$$ 映射到 $$w - {w_1, w_2}$$ 之后的新坐标为

$$X_{pr}^{(i)} = (X^{(i)}{pr1}, X^{(i)}{pr2})$$

那么, $$||x^{(i)}_{\text{project}}||$$ 为:

$$ ||x^{(i)}_{\text{project}}|| = X^{(i)} \cdot w $$

代入公式(3)得:

$$ \begin{aligned} Var(X_{\text{project}}) = \frac{1}{m}\sum_{i=1}^m|| X^{(i)} \cdot w||^2 && (4) \end{aligned} $$

目标是最大化公式(4),这是一个求目标函数的最优化问题,使用梯度上升法解决。

主成分分析法和线性回归的区别

| 主成分分析 | 线性回归 --|---|-- 坐标轴 | 2个特征 | 1个特征和输出标记 要求的是什么 | 一个方向 | 一根直线 经过点的线与什么垂直 | 所求的方向垂直 | x轴 目标 | 方差最大 | MSE最小

这是一个非监督学习算法,在式子中没有输出标记y

这是一个非监督学习算法,在式子中没有输出标记y

使用梯度上升法,就要先对目标函数求梯度,计算结果如下:

import numpy as np

import matplotlib.pyplot as plt

X = np.empty((100, 2))

X[:,0] = np.random.uniform(0., 100, size=100)

X[:,1] = 0.75 * X[:, 0] + 3. + np.random.normal(0, 10., size=100)

plt.scatter(X[:,0], X[:,1])

plt.show()

第一步:demean

def demean(X):

return X - np.mean(X, axis=0)

X_demean = demean(X)

plt.scatter(X_demean[:,0], X_demean[:,1])

plt.show()

第二步:梯度上升法

def f(w, X):

return np.sum((X.dot(w)**2)) / len(X)

def df_math(w, X):

return X.T.dot(X.dot(w)) * 2. / len(X)

def df_debug(w, X, epsilon=0.0001):

res = np.empty(len(w))

for i in range(len(w)):

w_1 = w.copy()

w_1[i] += epsilon

w_2 = w.copy()

w_2[i] -= epsilon

res[i] = (f(w_1, X) - f(w_2, X)) / (2 * epsilon)

return res

# 把向量单位化

def direction(w):

return w / np.linalg.norm(w)

def gradient_ascent(df, X, initial_w, eta, n_iters=1e4, epsilon=1e-8):

w = direction(initial_w)

cur_iter = 0

while cur_iter < n_iters:

gradient = df(w, X)

last_w = w

w = w + eta * gradient

w = direction(w)

if(abs(f(w, X)) - abs(f(last_w, X)) < epsilon):

break

cur_iter += 1

return w

注意1:epsilon取值比较小,因为w是方向向量,它的每个维度都很小,所以epsilon也要取很小的值

注意2:每次计算出w后要对其单位化

如果每次计算出w后不做单位化的工作,算法也可以工作,因为w本身也是代方向的。

但这样会导致搜索过程不顺畅。

因为如果不做单位化,w应该是公式要求的w偏大的,这就要求eta值非常小。

而eta值小又会导致循环次数非常多,性能就会下降。

因此遵循公式的假设条件,每次都让w成为方向向量。

训练和绘制结果

initial_w = np.random.random(X.shape[1])

eta = 0.001

gradient_ascent(df_debug, X_demean, initial_w, eta)

w = gradient_ascent(df_math, X_demean, initial_w, eta)

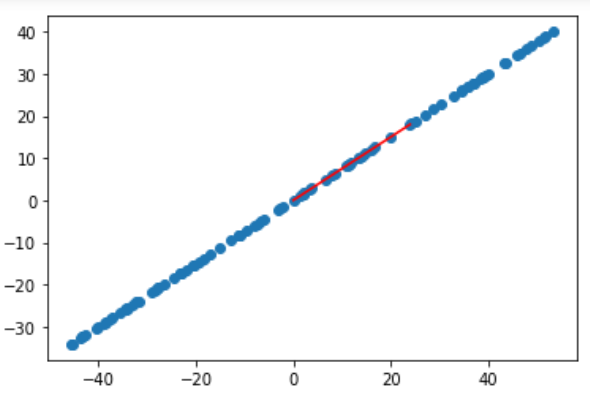

plt.scatter(X_demean[:, 0], X_demean[:, 1])

plt.plot([0, w[0]*30], [0, w[1]*30], color='r')

plt.show()

注意3:w不能是零向量。因为w=0本身也是在极值点上,是极小值点,此时梯度也会0

注意4:不能使用StandardScaler标准化数据。

因为本算法的目标就是让方差最大。

一但对数据做了标准化,样本的方差就肯定是1了,不存在方差最大值。

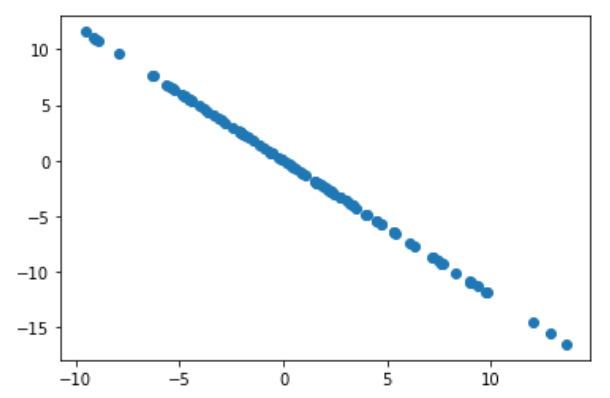

另一个更极端的例子

X2 = np.empty((100, 2))

X2[:,0] = np.random.uniform(0., 100, size=100)

X2[:,1] = 0.75 * X2[:, 0] + 3.

X2_demean = demean(X2)

w2 = gradient_ascent(df_debug, X2_demean, initial_w, eta)

plt.scatter(X2_demean[:, 0], X2_demean[:, 1])

plt.plot([0, w2[0]*30], [0, w2[1]*30], color='r')

plt.show()

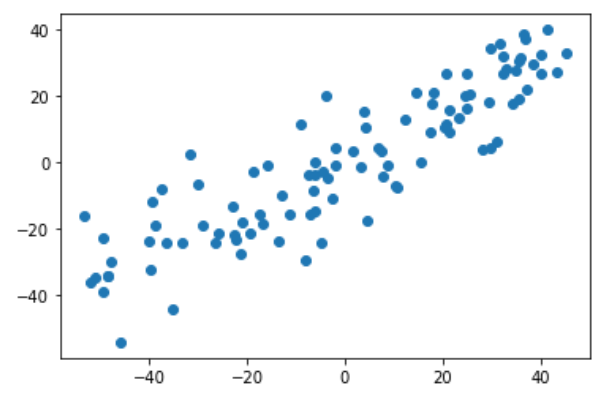

本质上是从一组坐标第转移到了另一组坐标系。 原来的坐标系有n个方向,那么新的坐标系也应该有n个方向。 7-2中的算法只是求出第一个轴的方向。

在新的坐标系中,第一个轴保存了样本最大的方差,称为第一个主成分。 第二个次之,依此类推。

问:求出第一主成分以后,如何求出下一主成分呢?

答:

第一步: 改变数据,将数据的第一个主成分去掉。

图中X'是X去除了第一主成分上的分量后的结果

第二步: 在新数据上求第一主成分

准备数据

import numpy as np

import matplotlib.pyplot as plt

X = np.empty((100, 2))

X[:,0] = np.random.uniform(0., 100, size=100)

X[:,1] = 0.75 * X[:, 0] + 3. + np.random.normal(0, 10., size=100)

plt.scatter(X[:,0], X[:,1])

plt.show()

第一步:demean

def demean(X):

return X - np.mean(X, axis=0)

X_demean = demean(X)

plt.scatter(X_demean[:,0], X_demean[:,1])

plt.show()

第二步:梯度上升法

def f(w, X):

return np.sum((X.dot(w)**2)) / len(X)

def df(w, X):

return X.T.dot(X.dot(w)) * 2. / len(X)

# 把向量单位化

def direction(w):

return w / np.linalg.norm(w)

def first_component(X, initial_w, eta, n_iters=1e4, epsilon=1e-8):

w = direction(initial_w)

cur_iter = 0

while cur_iter < n_iters:

gradient = df(w, X)

last_w = w

w = w + eta * gradient

w = direction(w)

if(abs(f(w, X)) - abs(f(last_w, X)) < epsilon):

break

cur_iter += 1

return w

训练和绘制结果

initial_w = np.random.random(X.shape[1])

eta = 0.001

w = first_component(X_demean, initial_w, eta)

输入:w

输出:array([0.77135006, 0.63641109])

第三步:去掉第一个主成分

方法一:

X2 = np.empty(X.shape)

for i in range(len(X)):

X2[i] = X[i] - X[i].dot(w) * w

方法二:

X2 = X - X.dot(w).reshape(-1, 1) * w

去掉第一主成分后的数据

plt.scatter(X2[:,0], X2[:,1])

plt.show()

第四步:求新数据的第一主成分

w2 = first_component(X2, initial_w, eta)

输入:w2

输出:array([-0.63639346, 0.77136461])

输入:w.dot(w2)

输出:2.2857453091384983e-05

点乘结果几乎为0,说明w和w2是垂直关系

封装成函数

def first_n_component(n, X, eta = 0.01, n_iters=1e4, epsilon=1e-8):

X_pca = X.copy()

X_pca = demean(X_pca)

res = []

for i in range(n):

initial_w = np.random.random(X.shape[1])

eta = 0.001

w = first_component(X_pca, initial_w, eta)

res.append(w)

X_pca = X_pca - X_pca.dot(w).reshape(-1, 1) * w

return res

输入:first_n_component(2, X)

输出:[array([0.77135082, 0.63641018]), array([ 0.63642749, -0.77133653])]

[?]遗留问题:我算出的第二个主成分的方向和视频中是反的?

可能是跟initial_w有关,多次运行后发现两个方向的结果都有。

定义:X是样本数据,每一行是一个数据,它有m个数据,每个数据有n个特征

$$

X =

\begin{bmatrix}

X_1^{(1)} && X_1^{(2)} && \cdots && X_1^{(n)} \

X_2^{(1)} && X_2^{(2)} && \cdots && X_2^{(n)} \

\cdots && \cdots && \cdots && \cdots \

X_m^{(1)} && X_m^{(2)} && \cdots && X_m^{(n)}

\end{bmatrix}

$$

$W_k$是求得的前k个主成分矩阵,每一行是一个主成分的单位方向,它有k个主成分方向,每个主成分的方向有n个维度

$$

X =

\begin{bmatrix}

W_k^{(1)} && W_1^{(2)} && \cdots && W_1^{(n)} \

W_2^{(1)} && W_2^{(2)} && \cdots && W_2^{(n)} \

\cdots && \cdots && \cdots && \cdots \

W_k^{(1)} && W_k^{(2)} && \cdots && W_k^{(n)}

\end{bmatrix}

$$

问:如何将样本X从N维转换成K维?

答:降维:把所有样本映射到K个主成分上

$$

X \cdot W_k^T = X_k

$$

还原:把降维后的数据还原到原坐标空间

$$

X_k \cdot W_k = X_m

$$

还原后的X与原X不同。

把PCA封装成类

import numpy as np

class PCA:

def __init__(self, n_components):

"""初始化PCA"""

assert n_components >= 1, "n_components must be valid"

self.n_components = n_components

self.components_ = None

def fit(self, X, eta=0.01, n_iters=1e4):

"""获取数据集的前n个主成分"""

assert self.n_components <= X.shape[1], "n_components must not be greater than the feature number of X"

def demean(X):

return X - np.mean(X, axis=0)

def f(w, X):

return np.sum((X.dot(w)**2)) / len(X)

def df(w, X):

return X.T.dot(X.dot(w)) * 2. / len(X)

# 把向量单位化

def direction(w):

return w / np.linalg.norm(w)

def first_component(X, initial_w, eta, n_iters=1e4, epsilon=1e-8):

w = direction(initial_w)

cur_iter = 0

while cur_iter < n_iters:

gradient = df(w, X)

last_w = w

w = w + eta * gradient

w = direction(w)

if(abs(f(w, X)) - abs(f(last_w, X)) < epsilon):

break

cur_iter += 1

return w

X_pca = demean(X)

self.components_ = np.empty(shape = (self.n_components, X.shape[1]))

for i in range(self.n_components):

initial_w = np.random.random(X.shape[1])

eta = 0.001

w = first_component(X_pca, initial_w, eta)

self.components_[i, :] = w

X_pca = X_pca - X_pca.dot(w).reshape(-1, 1) * w

return self

def transform(self, X):

"""将给定的X,映射到各个主成分分量中"""

assert X.shape[1] == self.components_.shape[1]

return X.dot(self.components_.T)

def inverse_transform(self, X):

"""将给定的X反向映射回原来的特征空间"""

assert X.shape[1] == self.components_.shape[0]

return X.dot(self.components_)

def __repr__(self):

return "PCA(n_components=%d)" % self.n_components

使用PCA降维

准备数据

import numpy as np

import matplotlib.pyplot as plt

X = np.empty((100,2))

X[:,0] = np.random.uniform(0., 100., size=100)

X[:,1] = 0.75 * X[:, 0] + 3. + np.random.normal(0, 10., size=100)

训练模型1

pca = PCA(n_components=2)

pca.fit(X)

输入:pca.components_

输出:array([[ 0.75366776, 0.65725559], [-0.65723751, 0.75368352]])

训练模型2:降维

pca = PCA(n_components=1)

pca.fit(X)

X_reduction = pca.transform(X)

X_restore = pca.inverse_transform(X_reduction)

输入:X_reduction.shape

输出:(100, 1)

输入:X_restore.shape

输出:(100, 2)

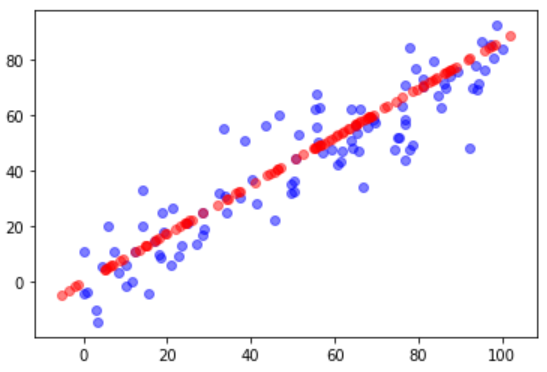

对比原始数据与降维再恢复后的数据

plt.scatter(X[:, 0], X[:, 1], color='b', alpha=0.5)

plt.scatter(X_restore[:, 0], X_restore[:, 1], color='r', alpha=0.5)

plt.show()

沿用7-5中的测试数据,使用scikit-learn中的PCA

from sklearn.decomposition import PCA

pca = PCA(n_components=1)

pca.fit(X)

输入:pca.components_

输出:array([[-0.75366744, -0.65725595]])

这个轴与7-5中的计算结果是相反的。因为scikit-learn中不是什么梯度下降法而是什么数学方法计算的。

轴的方向相反不影响算法的结果

对比原始数据与降维再恢复后的数据

X_reduction = pca.transform(X)

X_restore = pca.inverse_transform(X_reduction)

plt.scatter(X[:, 0], X[:, 1], color='b', alpha=0.5)

plt.scatter(X_restore[:, 0], X_restore[:, 1], color='r', alpha=0.5)

plt.show()

使用真实数据测试PCA降维对效率和准确度的影响

真实数据

import numpy as np

import matplotlib.pyplot as plt

from sklearn import datasets

digits = datasets.load_digits()

X = digits.data

y = digits.target

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, random_state=666)

几种降维结果比较

| PCA后的维数 | 运行时间 | score |

|---|---|---|

| 不降维 | 82.9 ms | 0.9866666666666667 |

| 2 | 2.2 | 0.6066666666666667 |

| 28 | 1,05 时间更少了? | 0.98 |

结论: 如果n_components选择合适,会大大减少训练时间而略微减少分类准确度,这样做是值得的。

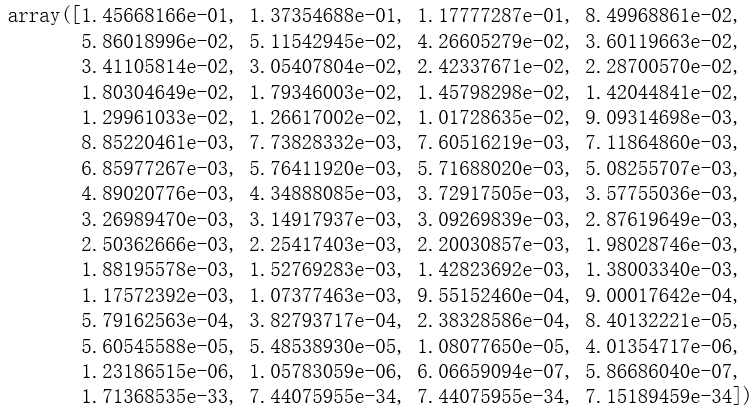

选择合适的降维效果

确定新坐标系中每个维度保存了原数据的方差百分比

pca = PCA(n_components=X_train.shape[1])

pca.fit(X_train)

pca.explained_variance_ratio_

输出结果:

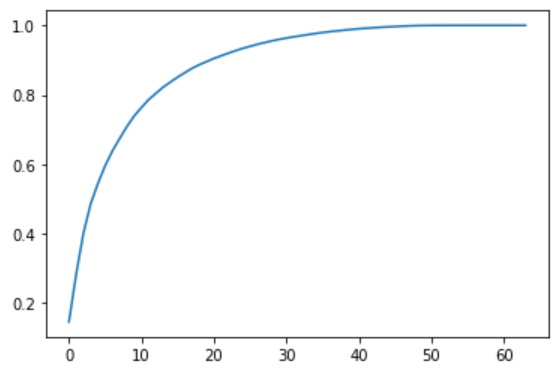

plt.plot([i for i in range(X_train.shape[1])],

[np.sum(pca.explained_variance_ratio_[:i+1]) for i in range(X_train.shape[1])])

plt.show()

输出结果:

这张图表示了前N个维度所占方差的百分比

保留原始数据95%的方差

pca = PCA(0.95)

pca.fit(X_train)

pca.explained_variance_ratio_

对原始数据降至2维的结果也有一定参考意义

pca = PCA(n_components=2)

pca.fit(X)

X_reduction = pca.transform(X)

for i in range(10):

plt.scatter(X_reduction[y==i, 0], X_reduction[y==i,1], alpha=0.8)

plt.show()

假如只是要区分图中紫色的数据和红色的数据,降到2维就足够了

使用sklearn提供的接口加载经典的MNIST手写数据集

import numpy as np

from sklearn.datasets import fetch_openml

mnist_data = fetch_openml("mnist_784")

X, y = mnist_data['data'], mnist_data['target'] # X.shape = (70000, 784)

X_train = np.array(X[:60000], dtype=float)

y_train = np.array(y[:60000], dtype=float)

X_test = np.array(X[60000:], dtype=float)

y_test = np.array(y[60000:], dtype=float)

KNN算法对MNIST分类

from sklearn.neighbors import KNeighborsClassifier

knn_clf = KNeighborsClassifier()

%time knn_clf.fit(X_train, y_train) # Wall time: 1min 3s

%time knn_clf.score(X_test, y_test) # Wall time = 15min 43, score = 0.9688

Note 1:

为什么KNN算法的fit要花费这么多时间?

因为当训练数据比较大的情况下,sklearn的KNN算法会使用tree来存储数据,而不是直接存储数据。

Note 2:

KNN算法通常需要对数据进行归一化,为什么这里没有做归一化?

因为当前的样本数据中,所有的特征都是表示图像中的像素点,整体处于同一个尺度,所以不需要归一化。

Note 3:

训练样本非常大的情况下,KNN算法非常耗时

PCA + KNN + MNIST

from sklearn.decomposition import PCA

pca = PCA(0.9)

pca.fit(X_train)

X_train_reduction = pca.transform(X_train) # X_train_reductionduction.shape = (60000, 784)

knn_clf = KNeighborsClassifier()

%time knn_clf.fit(X_train_reduction, y_train) # Wall time: 15.6 s

X_test_reduction = pca.transform(X_test)

%time knn_clf.score(X_test_reduction, y_test) # Wall time = 2min 20s, score = 0.8728

运行时间减少的同时,预测准确率反面提高了

PCA在降维的同时还可以降噪

之前的例子

原始数据:

import numpy as np

import matplotlib.pyplot as plt

X = np.empty((100,2))

X[:,0] = np.random.uniform(0., 100., size=100)

X[:,1] = 0.75 * X[:,0] + 3. + np.random.normal(0, 5, size=100)

plt.scatter(X[:, 0], X[:, 1])

plt.show()

降噪后:

from sklearn.decomposition import PCA

pca = PCA(n_components=1)

pca.fit(X)

X_reduction = pca.transform(X)

X_restore = pca.inverse_transform(X_reduction)

plt.scatter(X_restore[:, 0], X_restore[:, 1])

plt.show()

从图1到图2有信丢失了,丢失的这部分信息中很有可能有很大一部分是噪声 降维的过程中丢失了信息,同时也去除了部分噪音

手写识别例子

原始的手写数据:

from sklearn import datasets

digits = datasets.load_digits()

X = digits.data

y = digits.target

example_digits = X[y == 0, :][:10]

for num in range(1, 10):

X_num = X[y==num,:][:10]

example_digits = np.vstack([example_digits, X_num])

对原始的手写数据加噪

example_digits = example_digits + np.random.normal(0, 4, size=X.shape)

显示加噪后的图像:

def plot_digits(data):

#fig, axes = plt.subplots(10, 10, figsize=(10, 10), subplot_kw={'xticks':[], 'yticks':[]},girdspec_kw=dict(hspace=0.1, wspace=0.1))

fig, axes = plt.subplots(10, 10, figsize=(10, 10), subplot_kw={'xticks':[], 'yticks':[]})

for i,ax in enumerate(axes.flat):

ax.imshow(data[i].reshape(8, 8), cmap='binary', interpolation='nearest', clim=(0,16))

plt.show()

plot_digits(example_digits)

对example_digits去噪

pca = PCA(0.5)

pca.fit(noisy_digits) # pca.n_components_ = 12

components = pca.transform(example_digits)

filtered_digits = pca.inverse_transform(components)

去噪后的效果:

plot_digits(filtered_digits)

把W矩阵中的每一行看作一个方向,第一行代表最重要的方向,第二行代表次重要的方向,依次类推

也可以说:

将W矩阵中的每一行看作一个样本,第一行所代表的样本是最重要的样本,最能反应原X矩阵样本特征的样本。第二行所代表的样本是次重要的样本,依次类推。

X中的每一行都是一张人脸,W中的每一行也可以认为是一张脸,称为特征脸。每一个特征脸都是一个主成分,相当于表达了原样本数据的特征。(特征这个词与矩阵中的特征值这个词相对应)

取数据

import numpy as np

import matplotlib.pyplot as plt

from sklearn.datasets import fetch_lfw_people

faces = fetch_lfw_people()

random_indexes = np.random.permutation(len(faces.data))

X = faces.data[random_indexes]

查看图像:

def plot_faces(faces):

#fig, axes = plt.subplots(6, 6, figsize=(10, 10), subplot_kw={'xticks':[], 'yticks':[]},girdspec_kw=dict(hspace=0.1, wspace=0.1))

fig, axes = plt.subplots(10, 10, figsize=(10, 10), subplot_kw={'xticks':[], 'yticks':[]})

for i,ax in enumerate(axes.flat):

ax.imshow(data[i].reshape(62, 47), cmap='bone')

plt.show()

plot_faces(example_faces)

特征脸

from sklearn.decomposition import PCA

pca = PCA(svd_solver="randomized") #因为数据样本比较大,用随机的方式会快一些

%timeit pca.fit(X)

plot_faces(pca.components_[:36, :])

其它关于样本库

faces2 = fetch_lfw_people(min_faces_per_person=60) # 取一个人至少有60张照片的样本

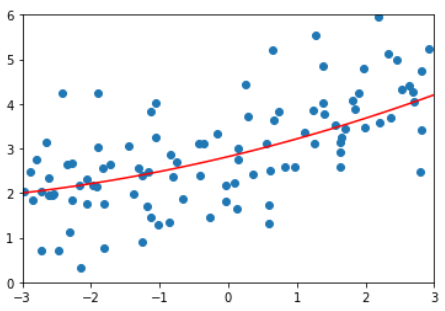

线性回归要求数据存在线性关系。

但实际场景中,存在强线性关系的数据是比较少的,大部分情况下数据之间是非线性关系。

用一种简单的手段改进线性回归法,使得它可以处理和预测非线性数据。

即多项式回归。

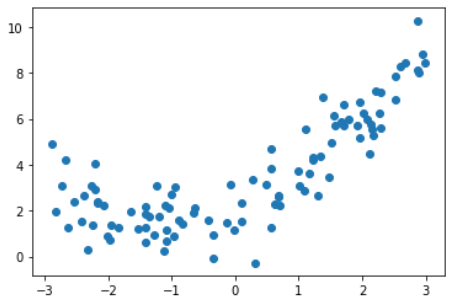

准备数据

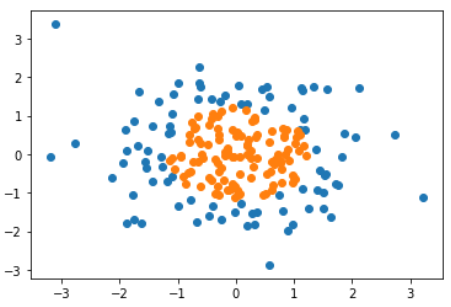

import numpy as np

import matplotlib.pyplot as plt

x = np.random.uniform(-3, 3, size=100)

X = x. reshape(-1, 1)

y = 0.5 * x**2 + x + 2 + np.random.normal(0, 1, size=100)

plt.scatter(X, y)

plt.show()

使用线性回归

from sklearn.linear_model import LinearRegression

lin_reg = LinearRegression()

lin_reg.fit(X, y)

y_predict = lin_reg.predict(X)

plt.scatter(x, y)

plt.plot(x, y_predict, color='r')

plt.show()

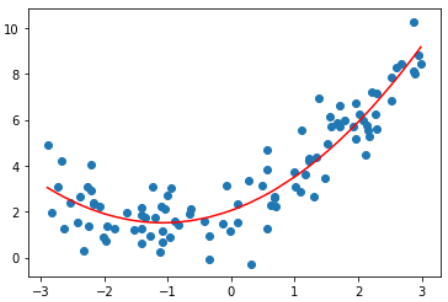

解决方案, 添加一个特征

X2 = np.hstack([X, X**2])

lin_reg2 = LinearRegression()

lin_reg2.fit(X2, y)

y_predict2 = lin_reg2.predict(X2)

plt.scatter(x, y)

plt.plot(np.sort(x), y_predict2[np.argsort(x)], color='r')

plt.show()

看上去这根曲线拟合得更好。

输入:lin_reg2.coef_

输出:array([0.99902653, 0.46334749])

0.999是x的系数,0.46是x^2的系数

输入:lin_reg2.intercept_

输出:2.0518267069340164

结论

使用线性回归的思路,为原来的样本添加新的特征,新的特征是原有特征的多项式的组合。以此来解决非线性问题。

PCA是对数据做降维处理,这里则是对数据集升维。通过升维和添加特征,使算法拟合高维度的数据。

线性回归要求数据存在线性关系。

但实际场景中,存在强线性关系的数据是比较少的,大部分情况下数据之间是非线性关系。

用一种简单的手段改进线性回归法,使得它可以处理和预测非线性数据。

即多项式回归。

准备数据

import numpy as np

import matplotlib.pyplot as plt

x = np.random.uniform(-3, 3, size=100)

X = x. reshape(-1, 1)

y = 0.5 * x**2 + x + 2 + np.random.normal(0, 1, size=100)

plt.scatter(X, y)

plt.show()

使用线性回归

from sklearn.linear_model import LinearRegression

lin_reg = LinearRegression()

lin_reg.fit(X, y)

y_predict = lin_reg.predict(X)

plt.scatter(x, y)

plt.plot(x, y_predict, color='r')

plt.show()

解决方案, 添加一个特征

X2 = np.hstack([X, X**2])

lin_reg2 = LinearRegression()

lin_reg2.fit(X2, y)

y_predict2 = lin_reg2.predict(X2)

plt.scatter(x, y)

plt.plot(np.sort(x), y_predict2[np.argsort(x)], color='r')

plt.show()

看上去这根曲线拟合得更好。

输入:lin_reg2.coef_

输出:array([0.99902653, 0.46334749])

0.999是x的系数,0.46是x^2的系数

输入:lin_reg2.intercept_

输出:2.0518267069340164

结论

使用线性回归的思路,为原来的样本添加新的特征,新的特征是原有特征的多项式的组合。以此来解决非线性问题。

PCA是对数据做降维处理,这里则是对数据集升维。通过升维和添加特征,使算法拟合高维度的数据。

准备数据

import numpy as np

import matplotlib.pyplot as plt

x = np.random.uniform(-3, 3, size=100)

X = x. reshape(-1, 1)

y = 0.5 * x**2 + x + 2 + np.random.normal(0, 1, size=100)

使用polynomialFeatures为原数据升维

from sklearn.preprocessing import PolynomialFeatures

poly = PolynomialFeatures(degree=2)

poly.fit(X)

X2 = poly.transform(X)

输入:X2.shape

输出:(100, 3)

输入:X2[:5,:]

输出:

array([[ 1. , -1.34284888, 1.80324311],

[ 1. , -0.18985858, 0.03604628],

[ 1. , -1.58563134, 2.51422675],

[ 1. , 1.2149354 , 1.47606802],

[ 1. , -2.05874706, 4.23843944]])

输入:X2[:5,:]

输出:

array([[-1.34284888],

[-0.18985858],

[-1.58563134],

[ 1.2149354 ],

[-2.05874706]])

X2中第一列是1,第二列是原数据,第三列是原数据的平方

使用scikit-learn中的线性回归算法

这一部分与8-1相同

from sklearn.linear_model import LinearRegression

lin_reg2 = LinearRegression()

lin_reg2.fit(X2, y)

y_predict2 = lin_reg2.predict(X2)

plt.scatter(x, y)

plt.plot(np.sort(x), y_predict2[np.argsort(x)], color='r')

plt.show()

输入:lin_reg2.coef_

输出:array([0. , 1.01723515, 0.46407147])

0是对X2是第一列数据拟合的结果

输入:lin_reg2.intercept_

输出:2.1789150996943945

关于PolynomialFeatures

X = np.arange(1,11).reshape(-1, 2)

poly = PolynomialFeatures(degree=2)

poly.fit(X)

X2 = poly.transform(X)

输入:X.shape

输出:(5, 2)

输入:X

输出:array([[ 1, 2], [ 3, 4], [ 5, 6], [ 7, 8], [ 9, 10]])

输入:X2.shape

输出:(5, 6)

输入:X2

输出:

array([[ 1., 1., 2., 1., 2., 4.],

[ 1., 3., 4., 9., 12., 16.],

[ 1., 5., 6., 25., 30., 36.],

[ 1., 7., 8., 49., 56., 64.],

[ 1., 9., 10., 81., 90., 100.]])

第一列:1,即0次幂

第二列:x1,1次幂

第三列:x2,1次幂

第四列:x1^2,2次幂

第五列:x1*x2,2次幂

第六列:x2^2,2次幂

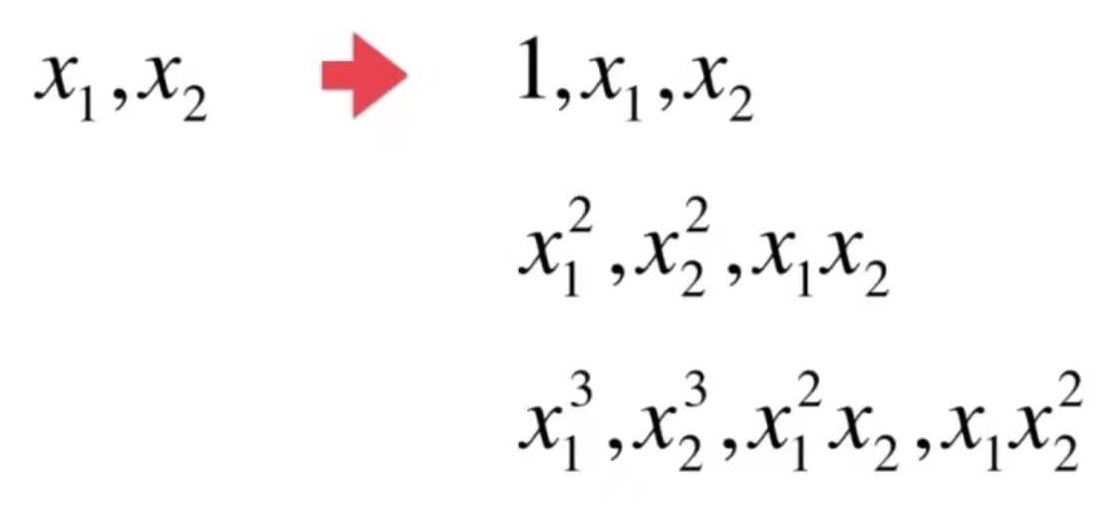

假设有x1, x2两个特征,PolynomialFeatures(degree=3),会得到多少项数据?

poly = PolynomialFeatures(degree=3)

poly.fit(X)

X3 = poly.transform(X)

# X3.shape = (5, 10)

# array([[ 1., 1., 2., 1., 2., 4., 1., 2., 4., 8.],

# [ 1., 3., 4., 9., 12., 16., 27., 36., 48., 64.],

# [ 1., 5., 6., 25., 30., 36., 125., 150., 180., 216.],

# [ 1., 7., 8., 49., 56., 64., 343., 392., 448., 512.],

# [ 1., 9., 10., 81., 90., 100., 729., 810., 900., 1000.]])

Pipeline

使用pipeline把多项式特征、数据规一化、线性回归三步合在一起,就不需要在每一次调用时都重复这三步

sklearn没有直接提供多项式回归算法,但可以使用pipe很方便地创建一个多项式回归算法

x = np.random.uniform(-3, 3, size=100)

X = x. reshape(-1, 1)

y = 0.5 * x**2 + x + 2 + np.random.normal(0, 1, size=100)

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LinearRegression

poly_reg = Pipeline([

("poly", PolynomialFeatures(degree=2)),

("std_scaler", StandardScaler()),

("lin_reg", LinearRegression())

])

poly_reg.fit(X, y)

y_predict = poly_reg.predict(X)

plt.scatter(x, y)

plt.plot(np.sort(x), y_predict[np.argsort(x)], color='r')

plt.show()

准备数据

import numpy as np

import matplotlib.pyplot as plt

x = np.random.uniform(-3, 3, size=100)

X = x. reshape(-1, 1)

y = 0.5 * x**2 + x + 2 + np.random.normal(0, 1, size=100)

使用线性回归

from sklearn.linear_model import LinearRegression

lin_reg = LinearRegression()

lin_reg.fit(X, y)

lin_reg.score(X, y) # score = 0.4953707811865009

y_predict = lin_reg.predict(X)

plt.scatter(x, y)

plt.plot(np.sort(x), y_predict[np.argsort(x)], color='r')

plt.show()

from sklearn.metrics import mean_squared_error

y_predict = lin_reg.predict(X)

mean_squared_error(y, y_predict)

均方误差为:3.0750025765636577

使用多项式回归

多项式回归算法

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import PolynomialFeatures

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LinearRegression

def PolynomialRegression(degree):

return Pipeline([

("poly", PolynomialFeatures(degree=degree)),

("std_scaler", StandardScaler()),

("lin_reg", LinearRegression())

])

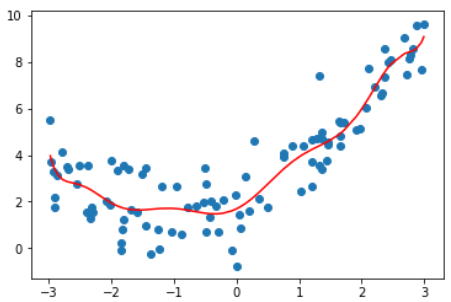

degree = 2的多项式回归

poly2_reg = PolynomialRegression(degree=2)

poly2_reg.fit(X, y)

y2_predict = poly2_reg.predict(X)

mean_squared_error(y, y2_predict) # 1.0987392142417856

y_predict = lin_reg.predict(X)

plt.scatter(x, y)

plt.plot(np.sort(x), y2_predict[np.argsort(x)], color='r')

plt.show()

degree取不同值得到的均方误差和拟合结果

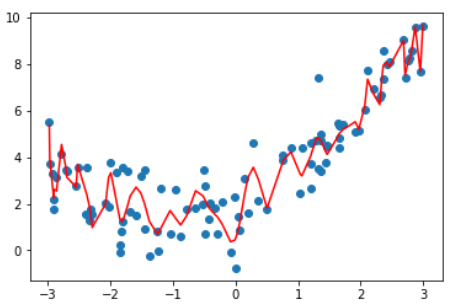

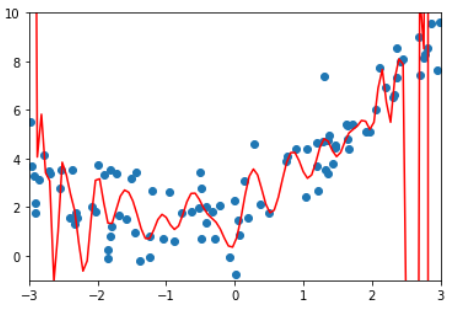

| degree | MSE | plot |

|---|---|---|

| 线性 | 3.0750025765636577 | |

| 2 | 1.0987392142417856 | |

| 10 | 1.050846676376417 |  |

| 100 | 0.6880004678712686 |  |

这张图不是特别准确,因为这根曲线只是原有数据点连接出来的结果.

因为有些x点取不到,不能准确描述所有点的y值,

均匀取值x并绘制图像如下

显示这不是我们想要的曲线。

结论:degree越高,对训练样本的拟合越好。

因为当degree足够大,总能找到一根曲线拟合所有的样本点,使得均方误差为0.

虽然拟合结果的均方误差小了,但它并没有真的反应样本点的曲线走势。

它为了拟合所有给定的样本而变得太过复杂,这就是过拟合(over fitting)

相反,如果只是使用一根直线来拟合样本数据,也没有很好的拟合样本的特征。

但它不是太复杂了,而是太简单了,这就是欠拟合(under fitting)

机器学习主要要解决的问题是过拟合问题。

例如这根曲线,虽然这根曲线将样本点拟合得很好,总体误差很低,但如果来了一个新样本,它就不能进行很好的预测了。也就是说,这个模型的泛能力很弱。

泛化能力即由此及彼的能力。

我们训练模型不是为了这些已知的点,而是为也预测。因此模型对训练数据的拟合程度有多好是没有意义的。真正需要的是模型的泛化能力。

解决方法:

训练、测试数据分离。

模型只使用训练数据集获取。测试数据对于模型是全新的数据。

如果模型对于测试数据也有很好的结果,就说模型的泛化能力是很强的。

如果模型对训练数据集的效果好,而对测试数据的效果很差,就说模型的泛化能力很弱,通常是过拟合。

仍使用8-3的数据,degree取不同值时在test数据集上的效果对比

| degree | 在训练数据集上的MSE | 在测试数据集上的MSE | note |

|---|---|---|---|

| 线性 | 3.0750025765636577 | 2.2199965269396573 | |

| 2 | 1.0987392142417856 | 0.80356410562979 | 使用二次模型得到的泛化结果比使用线性模型得到的要好 |

| 10 | 1.050846676376417 | 0.9212930722150768 | 在训练数据集上(8-3)degree取10效果更好,但在测试数据集上degree取10的效果变差了。说明degree取10时它的泛化能力变弱了。 |

| 100 | 0.6880004678712686 | 14075796434.50641 | 在训练数据集上效果最好,在测试数据集上效果极差 |

测试数据集的意义

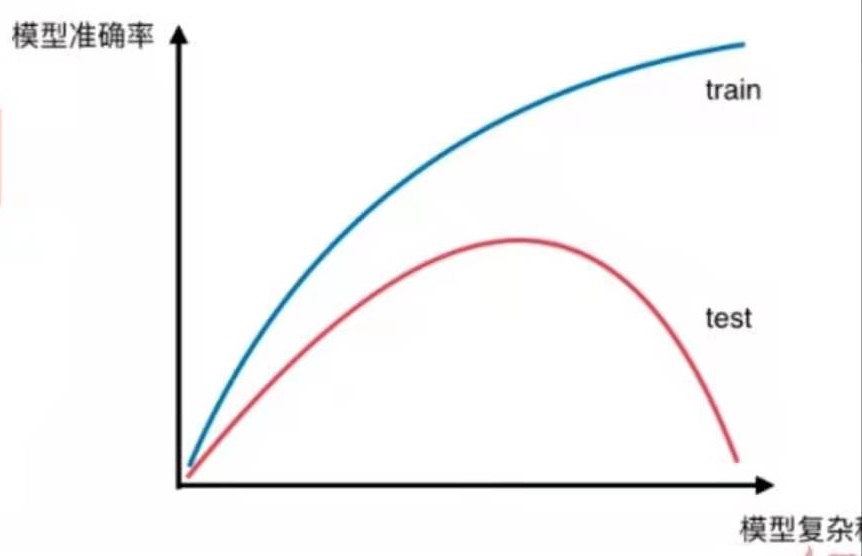

对于不同的算法,模型复杂度代码不同的意思。

对于多项式回归算法来说,模型复杂度相当于degree,degree越高,模型越复杂。

对于KNN算法来说,K越小,模型越复杂。

如图所示:

对于训练数据来说,模型越复杂,模型准确率就越高。

对于测试数据来说,模型最简单时,测试数据的准确率会比较低,当模型变复杂时,训练数据的准确率会提升。随着模型越来越复杂,当准确率提升到一定程度时又开始下降。

这就是“欠拟合-合适-过拟合”的过程。

这只是一个示意图,不同模型得到的具体图像不同,但整体上是这样的趋势。

欠拟合 vs 过拟合

欠拟合 underfitting

算法所训练的模型不能完整表述数据关系。

过拟合 overfitting

算法所训练的模型过多地表达了数据间的噪音关系。

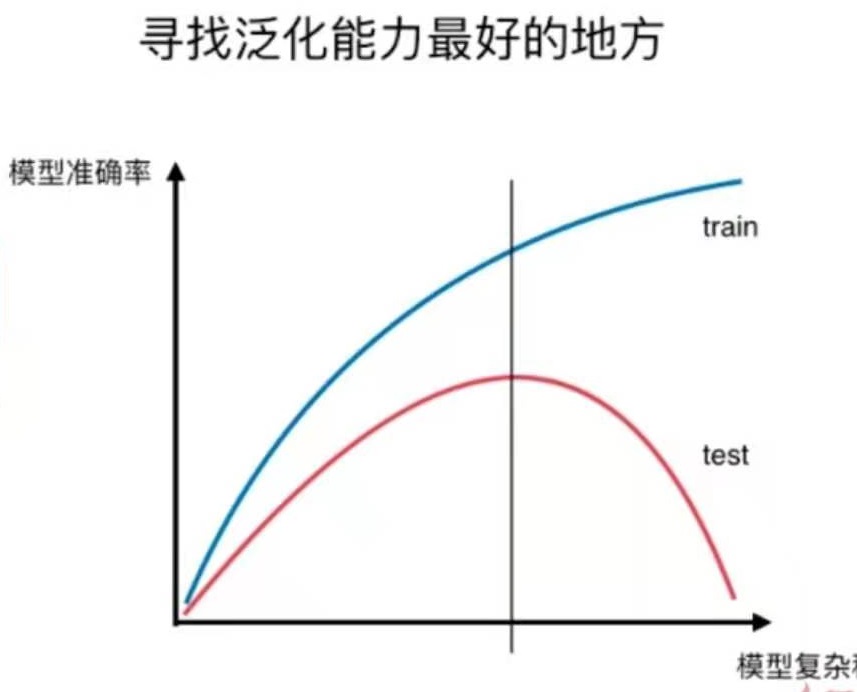

这是8-4中提到的模型复杂度曲线。用于说明过拟合和欠拟合。

还有另一种曲线,也可以可视化地表达过拟合与欠拟合的情况,即学习曲线。

学习曲线

随着训练样本的逐渐增多,算法训练出的模型的表现能力。

欠拟合、拟合、过拟合和学习曲线图对比

仍使用8-4中的数据

绘制学习曲线的函数如下:

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_squared_error

def plot_learning_curve(algo, X_train, X_test, y_train, y_test):

train_score = []

test_score = []

for i in range(1, len(X_train)+1):

algo.fit(X_train[:i], y_train[:i])

y_train_predict = algo.predict(X_train[:i])

train_score.append(mean_squared_error(y_train[:i], y_train_predict))

y_test_predict = algo.predict(X_test)

test_score.append(mean_squared_error(y_test, y_test_predict))

plt.plot([i for i in range(1, len(X_train)+1)], np.sqrt(train_score), label="train")

plt.plot([i for i in range(1, len(X_train)+1)], np.sqrt(test_score), label="test")

plt.legend()

plt.axis([0, len(X_train)+1, 0, 4])

plt.show()

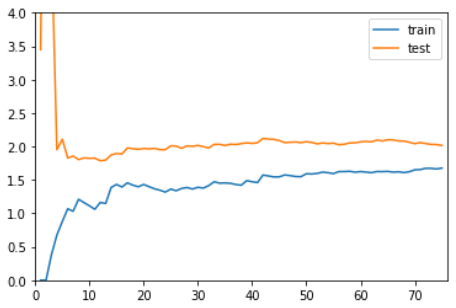

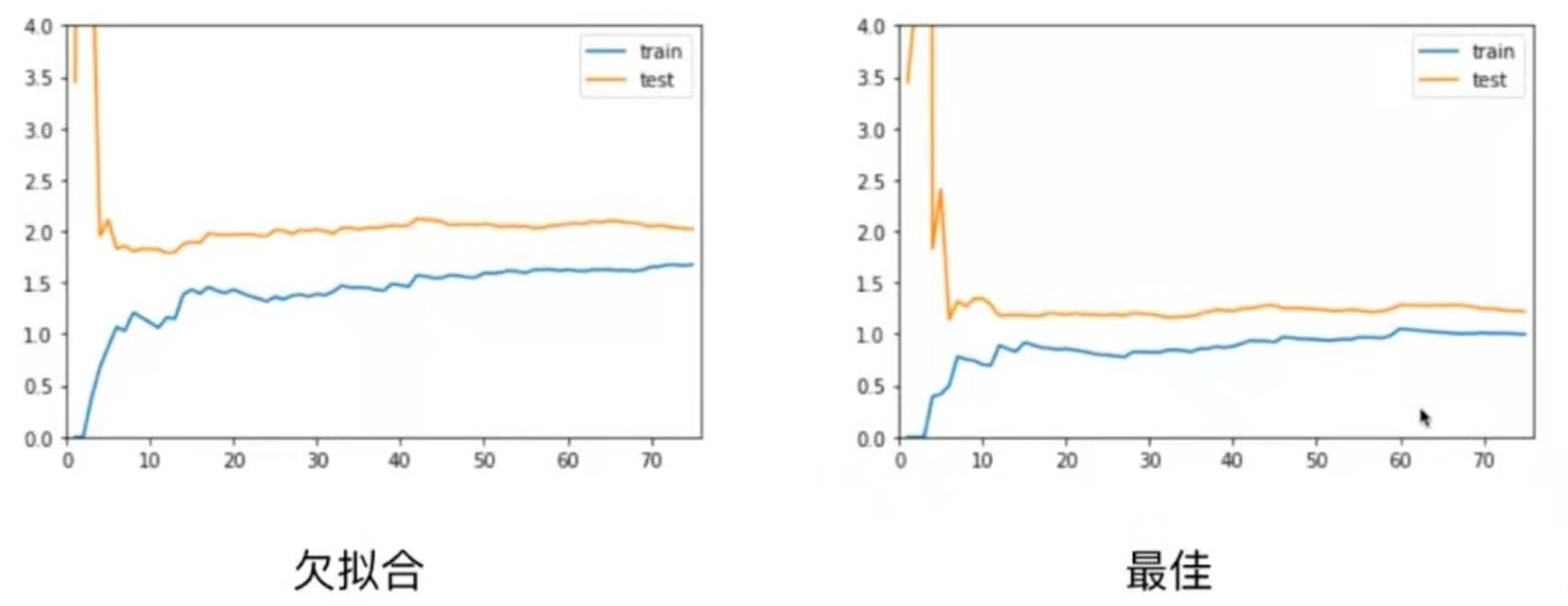

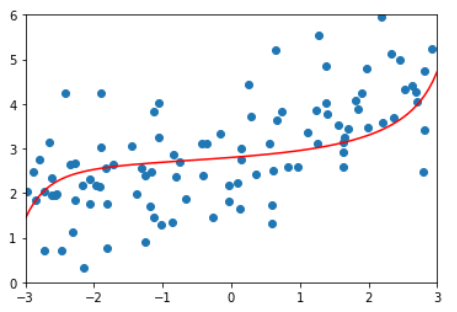

线性回归,欠拟合

plot_learning_curve( LinearRegression(), X_train, X_test, y_train, y_test)

在训练数据集上,误差逐渐升高。

刚开始,误差累积较快,到后面误差累积变慢。

在测试数据集上,刚开始误差很大,逐渐减小,减小到一定程度后达到相对稳定。

最终,训练误差与测试误差趋于大体相同。测试误差略高于训练误差。

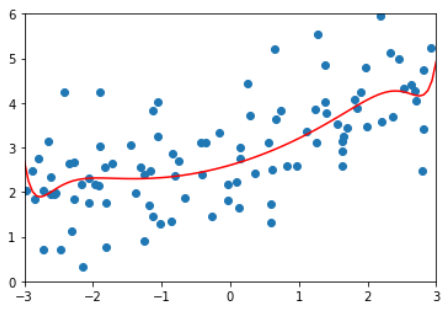

2阶多项式回归,拟合

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import PolynomialFeatures

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LinearRegression

def PolynomialRegression(degree):

return Pipeline([

("poly", PolynomialFeatures(degree=degree)),

("std_scaler", StandardScaler()),

("lin_reg", LinearRegression())

])

plot_learning_curve( PolynomialRegression(degree=2), X_train, X_test, y_train, y_test)

整体趋势与使用线性回归的图像是一致的。

区别在于,线性回归模型中训练误差和测试误差稳定在1.7左右

而2阶多项式回归模型中训练误差和测试误差稳定在1.0左右

这说明使用2阶多项式回归的结果是比较好的。

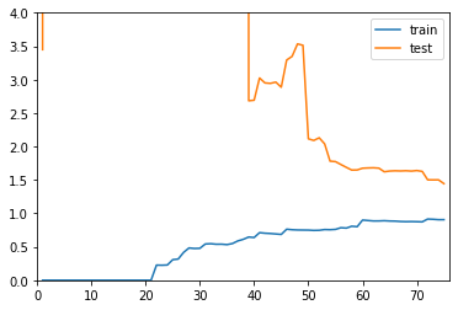

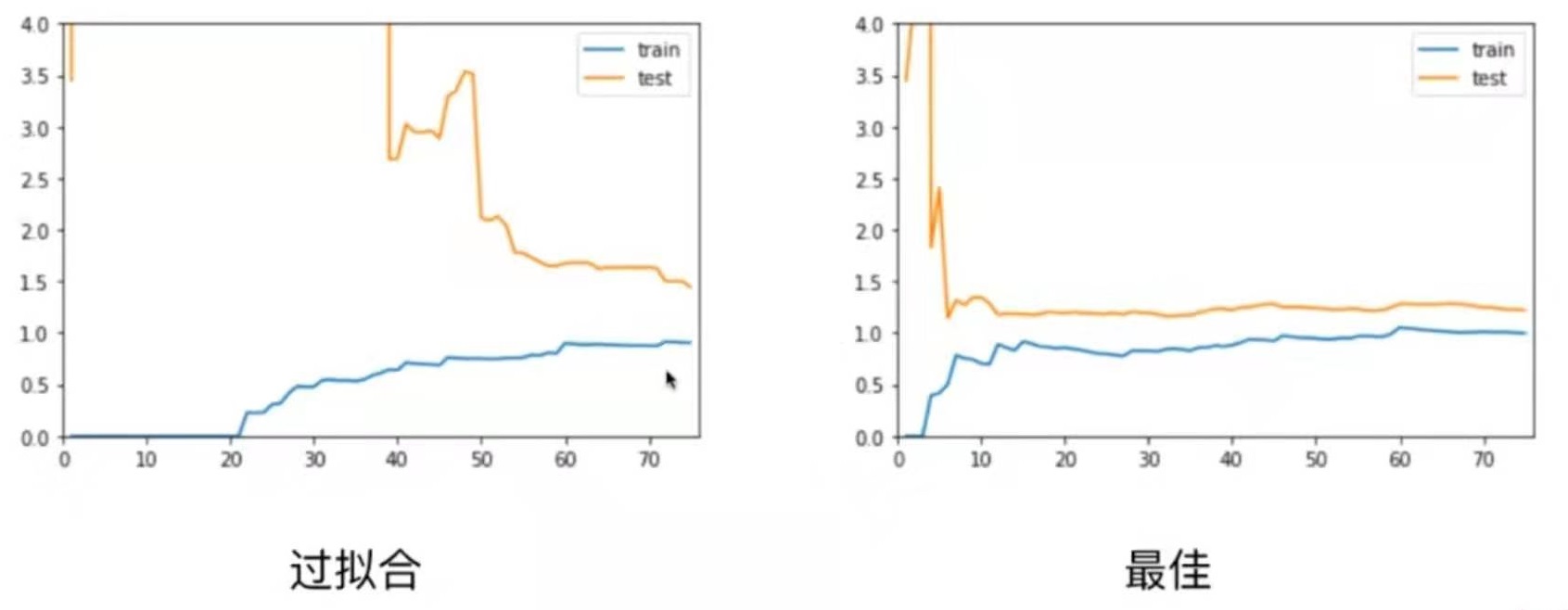

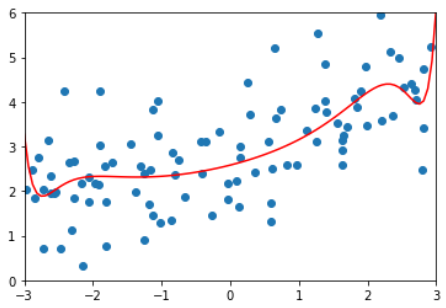

20阶多项式回归,过拟合

plot_learning_curve( PolynomialRegression(degree=20), X_train, X_test, y_train, y_test)

整体趋势仍然是train逐渐上升,test逐渐下降,最终趋于稳定。

在区别是,在train和test都比较稳定时,它们之间的差距是比较大。

这就说明模型虽然在训练数据集上拟合得非常好,但是在测试数据集上误差仍然很大。

这种情况通常就是过拟合。

总结

欠拟合情况和最佳情况相比,欠拟合情况train、test曲线趋于稳定的位置比最佳情况的要高一些。这是因为模型选择得不对,所以即使在训练数据集上误差也很大。

欠拟合情况和最佳情况相比,欠拟合情况train、test曲线趋于稳定的位置比最佳情况的要高一些。这是因为模型选择得不对,所以即使在训练数据集上误差也很大。

对于过拟合情况,train曲线和最佳情况差不多,但test曲线比较高,并且train与test之间的差距比较大。

对于过拟合情况,train曲线和最佳情况差不多,但test曲线比较高,并且train与test之间的差距比较大。

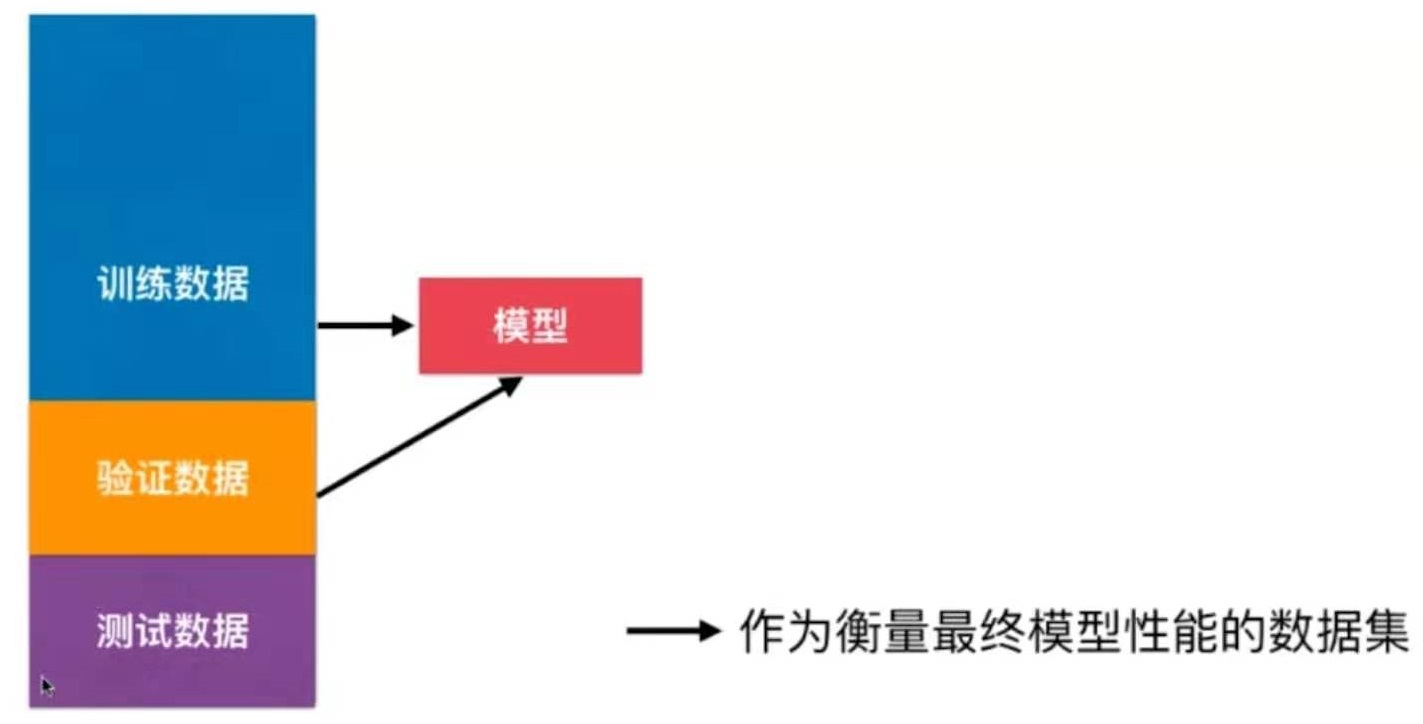

问题:发生了过拟合成不自知

解决方法:train test split

训练数据集:训练模型

测试数据集:调整超参数

问题:针对特定测试数据集过拟合?

解决方法:训练 - 验证 - 测试

训练数据集:训练模型

验证数据集:调整超参数

测试数据集:不参数模型创建,作为衡量最终模型性能的数据集

问题:随机?一旦验证数据集有异常数据,就会导致模型不准确

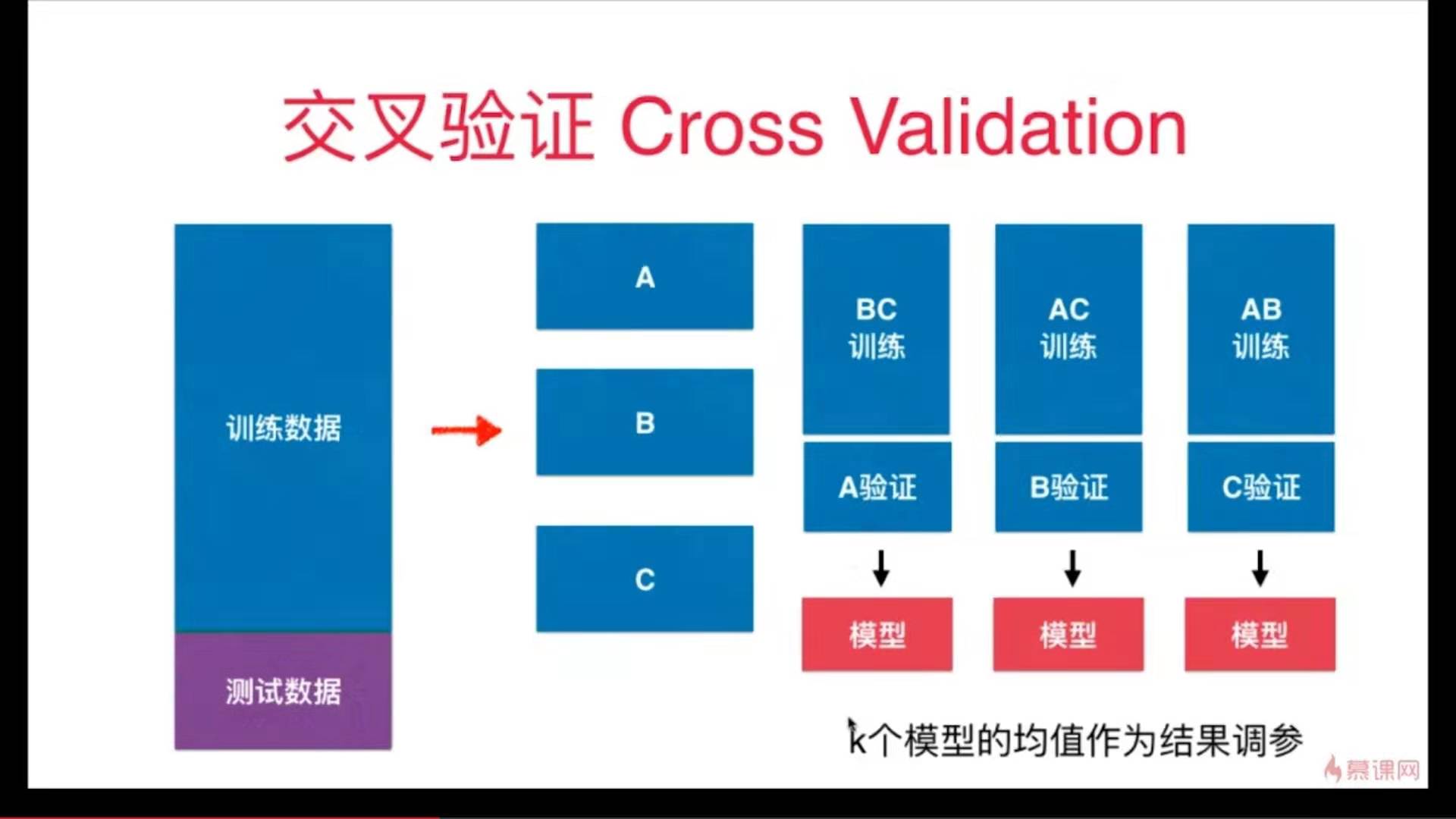

解决方法:交叉验证

代码实现

import numpy as np

from sklearn import datasets

digits = datasets.load_digits()

X = digits.data

y = digits.target

测试train_test_split

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.4, random_state=666)

from sklearn.neighbors import KNeighborsClassifier

best_score, best_k, best_p = 0,0,0

for k in range(2, 11):

for p in range(1, 6):

knn_clf = KNeighborsClassifier(weights="distance", n_neighbors=k, p=p)

knn_clf.fit(X_train, y_train)

score = knn_clf.score(X_test, y_test)

if score > best_score:

best_score, best_k, best_p = score, k, p

print("best k = ", best_k)

print("best p = ", best_p)

print("best score = ", best_score)

输出结果:

best k = 3

best p = 4

best score = 0.9860917941585535

使用交叉验证

from sklearn.model_selection import cross_val_score

knn_clf = KNeighborsClassifier()

cross_val_score(knn_clf, X_train, y_train)

输出结果:

array([0.98895028, 0.97777778, 0.96629213])

from sklearn.neighbors import KNeighborsClassifier

best_score, best_k, best_p = 0,0,0

for k in range(2, 11):

for p in range(1, 6):

knn_clf = KNeighborsClassifier(weights="distance", n_neighbors=k, p=p, cv=3)

scores = cross_val_score(knn_clf, X_train, y_train)

score = np.min(scores)

if score > best_score:

best_score, best_k, best_p = score, k, p

print("best k = ", best_k)

print("best p = ", best_p)

print("best score = ", best_score)

输出结果:

best k = 2

best p = 2

best score = 0.9823599874006478

train_test_split和交叉验证结果对比:

两种方法得到的best_k和best_p,通常认为使用交叉验证得到参数更可靠。

因为方法一得到的结果很有可能只是过拟合了那一组测试数据。

方法二的分数低于方法一,因为它没有过拟合某一组数据。

best_knn_clf = KNeighborsClassifier(weights="distance", n_neighbors=2, p=2)

best_knn_clf.fit(X_train, y_train)

best_knn_clf.score(X_test, y_test)

输出结果:0.980528511821975

Note:这个算法最终的分类准确度不是上面的0.9823,而是这里的0.9805

回顾网格搜索

from sklearn.model_selection import GridSearchCV

param_grid = [

{

'weights':['distance'],

'n_neighbors': [i for i in range(2, 11)],

'p': [i for i in range(1, 6)]

}

]

from sklearn.neighbors import KNeighborsClassifier

knn_clf = KNeighborsClassifier()

grid_search = GridSearchCV(knn_clf, param_grid, cv=3)

grid_search.fit(X_train, y_train)

输入:grid_search.best_score_

输出:0.9823747680890538

输入:grid_search.best_params_

输出:{'n_neighbors': 2, 'p': 2, 'weights': 'distance'}

输入:

best_knn_clf = grid_search.best_estimator_

best_knn_clf.score(X_test, y_test)

输出:0.980528511821975

使用网络搜索与使用交叉验证得到的结果相同。

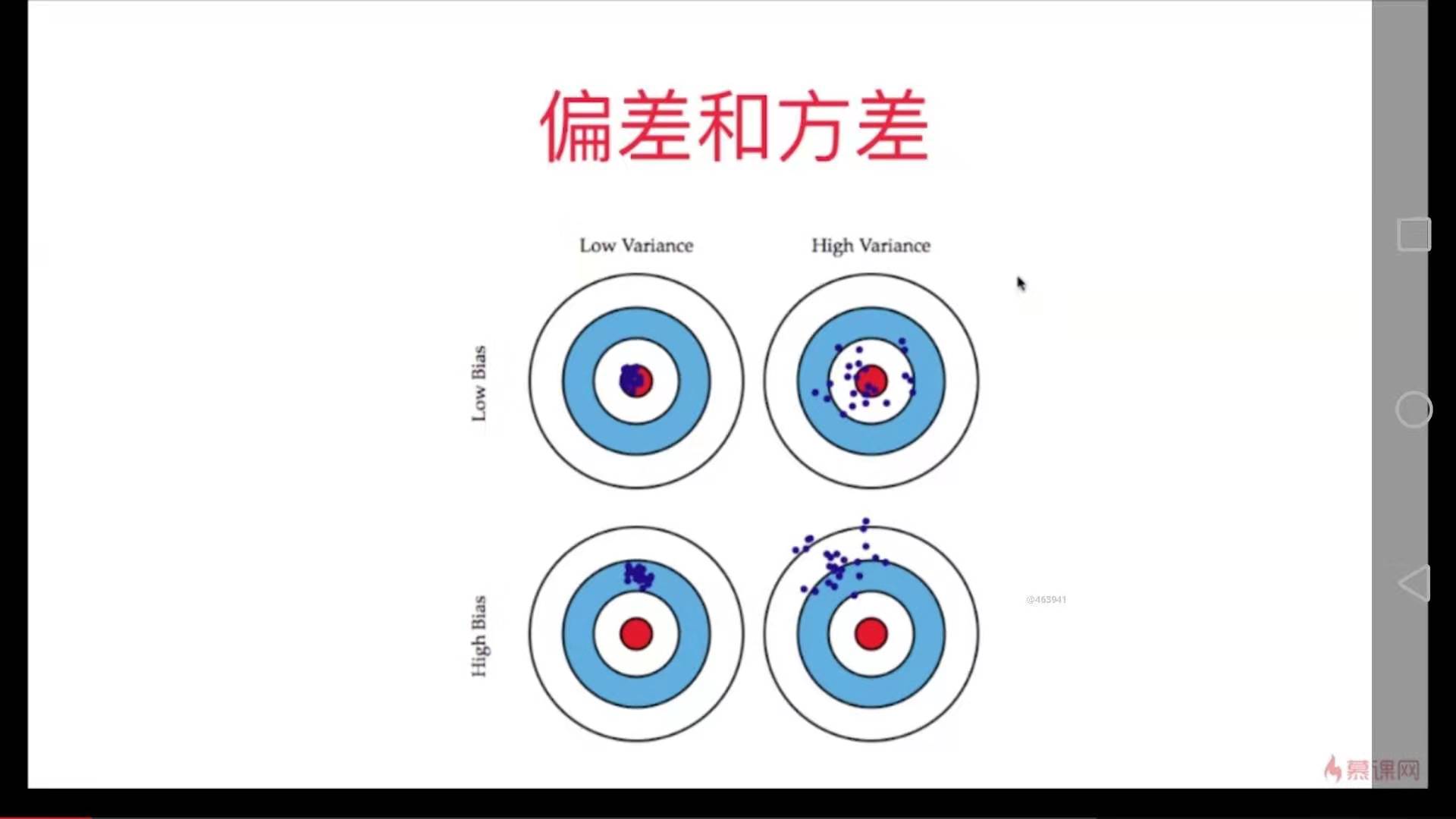

把要解决的问题看作是这个靶盘,训练的模型看作是打出去的枪。

模型的误差 = 偏差 + 方差 + 不可避免的误差

偏差 Bias

导致偏差的原因:

对问题本身的假设不正确。如:非线性数据使用线性回归

欠拟合 underfitting

特征选择不正确

方差 Variance

数据的一点点扰动都会较大地影响模型。

通常原因,使用的模型太复杂,如高阶多项式回归

过拟合 overfitting

偏差和方差

有一些算法天生是高方差的算法。如KNN。

非参数学习算法通常都是高方差算法,因为不对数据做任何假设。

有一些算法天生是高偏差算法。如线性回归。

参数学习算法通常都是高偏差算法。因为对数据有极强的假设性。

大多数算法具有相应的参数,可以调整偏差和方差。 例如KNN中的K、如多项式回归中的degree。

偏差和方差通常是矛盾的。降低偏差,会提高方差。降低方差会提高偏差。

在算法层面上,机器学习的主要挑战来自方差。

解决高方差的通常手段:

- 降低模型复杂度

- 减少数据维度,降噪

- 增加样本数

- 使用验证集

- 模型正则化

模型正则化:限制参数的大小

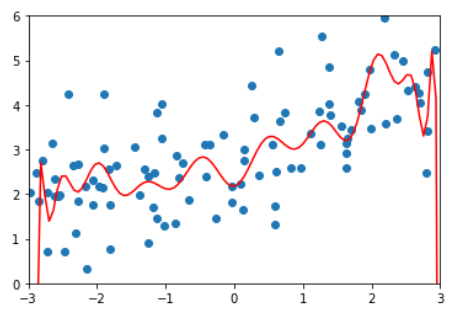

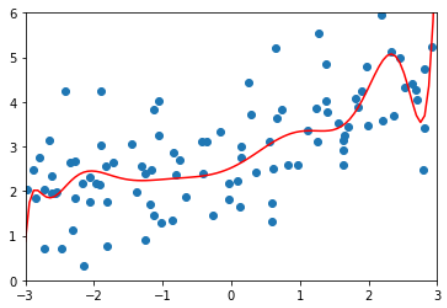

一个过拟合的例子:

这是8-3中的一个过拟合的例子,把模型的参数打出来如下:

为了尽量地拟合数据,使得线条非常陡峭,数学上表示就是系数非常大

岭回归 Ridge Regularization

Note 1: 正则项是从1累加到n的,theta 0不在里面,因为theta 0代表偏移,不是真正的系数。

Note 2:系数1/2加不加都可以,加了是为了求导方便。

Note 3:a是一个新的超参数,表示目标函数中模型正则化的程度。

代码实现

测试数据

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(42)

x = np.random.uniform(-3.0, 3.0, size=100)

X = x.reshape(-1, 1)

y = 0.5 * x + 3 + np.random.normal(0, 1, size=100)

plt.scatter(X, y)

plt.show()

多项式回归,degree = 20

训练模型

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import PolynomialFeatures

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LinearRegression

def PolynomialRegression(degree):

return Pipeline([

("poly", PolynomialFeatures(degree=degree)),

("std_scaler", StandardScaler()),

("lin_reg", LinearRegression())

])

from sklearn.model_selection import train_test_split

np.random.seed(666)

X_train, X_test, y_train, y_test = train_test_split(X, y)

from sklearn.metrics import mean_squared_error